Digital disruptors and bold innovators are reshaping South Africa’s banking sector

The banking industry in South Africa has always had an excellent reputation, both locally and internationally, with a total asset base of approximately R8.2tn, which is larger than the country’s entire annual GDP. The industry is still dominated by four big banks, with Capitec Bank making great strides, having secured the largest retail customer base, but remaining comparatively small in terms of total assets. There have been some developments in the sector, including the relaunch of YWBN Mutual Bank as eNL Mutual Bank – the first majority black women-owned bank founded by Nthabeleng Likotsi – signalling a transformation towards a more inclusive South African banking industry.

Global markets and the survival of South Africa’s banking system.

Perhaps aided by foreign exchange controls, South African banks escaped the astronomical losses incurred by banks from the subprime crisis in the US, Europe, and, to a lesser extent, Asia. The crisis resulted in some banks going bankrupt and others being bailed out by their governments for billions of dollars.

Market trends and growth of the banking sector

Sizeable private South African banks are steadily increasing in number, with Investec, Capitec, TymeBank and Discovery Bank joining the fray while maintaining the high standard of good financial standing and reputation. The attack by an American investment house on Capitec a few years back caused a ripple but quickly faded, with the Financial Sector Conduct Authority later finding that the Viceroy report was false and fining the firm. This demonstrates a strong and effective regulatory framework.

A noteworthy observation about the South African financial sector is the success of Capitec Bank business model, which caught the financial community by surprise. The bank, in a matter of a few years, now has the largest branch network, whereas the other major banks went on a drive to reduce their branch networks to cut costs. Despite the number of branches, Capitec achieved the lowest cost-to-income ratio at about 10 percentage points lower than other major banks, with a return on capital that is nine percentage points higher than the next big bank. Equity investors, who represent an aggregate of many opinions, rewarded Capitec with a very high market capitalisation.

The older banks follow traditional business models and are therefore slow to think out of the box. Capitec took a bold approach, entering a market segment that traditional banks avoided, achieving high profitability on a much lower asset base.

Old Mutual felt challenged to emulate Capitec by launching a new bank styled on Capitec’s business model.

How competition is benefiting customers

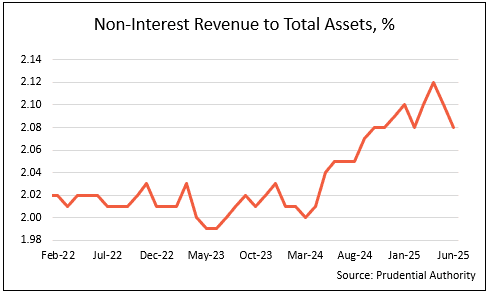

Another noteworthy observation is the increase in digital banking in South Africa, which put the brakes on the major banks extracting higher non-interest income from their customer base, as shown in Who Owns Whom’s report on the South African banking industry.

Digital banks can offer low- or no-cost banking because they have little or no physical retail infrastructure, though some, like Discovery Bank, target niche markets and are more expensive than their fintech peers. TymeBank had 10.7 million customers and R11.1bn assets in 2024. Discovery Bank had 1.4m customers and R30.2bn assets. Overall, the TymeBank model of low infrastructure costs – no branches- and low transaction costs prevails in the fintech market in South Africa. While interest in the South African financial services sector waned slightly over the last few years due to the country’s grey listing, some international fintechs, such as Revolut, are now showing interest in setting up business in South Africa, despite foreign exchange control restrictions and hurdles.

The impact of economic growth and fiscal management on the banking sector

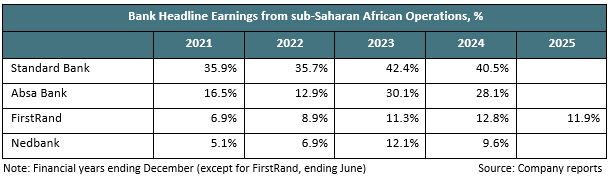

The Who Owns Whom report indicates that the country’s low economic growth has affected the banking industry, leading big banks to increasingly turn to other countries on the African continent for growth. Expanding into sub-Saharan Africa has been a key focus of South African banks. The table below reflects the growing contributions:

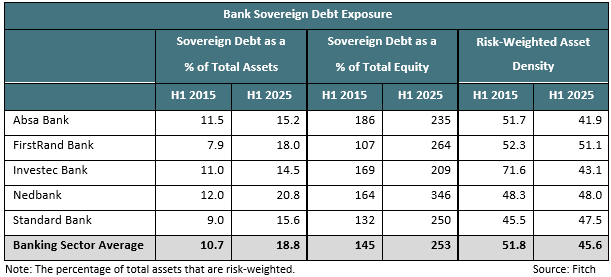

South Africa’s mainstream media hardly covers the extent of the banking sector’s sovereign debt exposure, which is quite significant, as illustrated in the table.

There are advantages to investing in high-yield, low-risk government assets, but this might not be sustainable in the future, given government’s high deficits. There have been promises of debt stabilisation in the past, which have not been followed through on, resulting in some loss of credibility. Government must strengthen its fiscal discipline to reduce vulnerability.

While the banking industry remains resilient, slow growth and rising sovereign exposure signal a shift in the sector as digital banking disrupts traditional models. Opportunities remain open for small players and fintech innovators to target underserved markets, offer low-cost services and specialise in niche financial solutions.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

Blog South AfricaTransportation & Logistics

South Africa’s air transport and aviation’s re-mergence, its struggles and opportunities.

Contents [hide] The Who Owns Whom report on air transport and aviation ground-handling services in South Africa highlights the paradox of how a powerful economic enabler that drives tourism, trade,...

Blog South Africa

Beyond the grave, and the evolution of culture in the funeral services industry in South Africa

Contents [hide] Funeral services and related industries have undergone a gradual transformation since the advent of democracy in 1994 from a community-based, culturally driven sector into a complex, multi-billion-rand industry...

Blog Public administration and defence compulsory social security

South Africa’s defence capability, performance, partners and rising global risks

Contents [hide] The Russia-Ukraine war is demonstrating how agile, technology-driven warfare dominated by drones, missiles and precision systems is starting to undermine traditional on-the-ground troops and heavy equipment. South Africa’s...