Can South Africa turn its chrome dominance into industrial power?

South Africa’s iron ore and chrome mining sector has benefited from the recent commodity price boom, strengthening export earnings and stimulating new investment. Yet beneath this growth lie challenges in beneficiation, electricity costs, and global competition that are shaping the outlook for chrome and ferrochrome production.

Major Producers Commit Billions to Chrome Growth Projects

Chrome is vital to the global economy, and is the primary input in stainless steel production, boosting strength, resistance and durability. It is therefore crucial to construction, automotive manufacturing, energy infrastructure and industrial equipment worldwide.

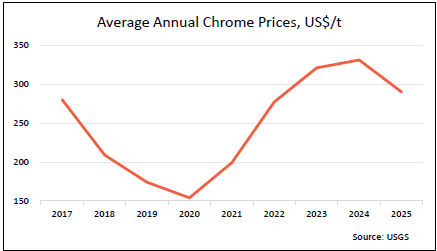

Chrome producers are taking advantage of higher prices while taking a long-term view on the commodity by investing in their mines and chrome recovery plants to increase production. Eight major investments, totalling billions of rands, are in the pipeline to increase chrome production. Among them are Tharisa, Impala Bafokeng mine, African Rainbow Minerals, Mantengu, the 50:50 Thaba JV between Limberg Mining Company and London Stock Exchange-listed Sylvania Platinum.

While this is beneficial for South Africa, especially since chrome is a foreign-exchange earner, some issues cannot be overlooked amid this good news.

Chrome and ferrochrome sector challenges

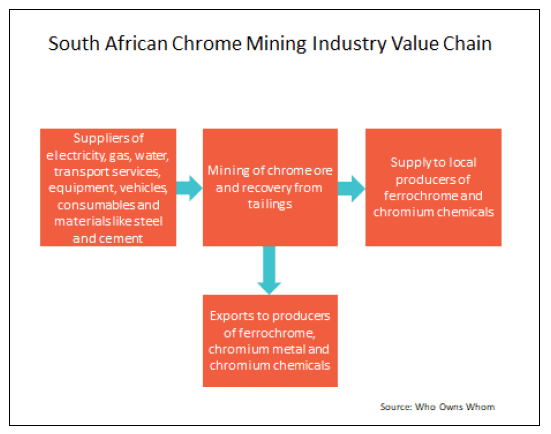

South Africa was the world’s largest producer of chrome ore and concentrate in 2025, producing an estimated 23.6 million tonnes (Mt), representing 45.8% of the global total. South Africa also has plenty of iron ore, the basic component of steelmaking, as stated in the Who Owns Whom report on Mining of Iron Ore and Chrome in South Africa. However, the country has not achieved the beneficiation goals articulated in its policies. This is due to high electricity costs and supply instability, limited local smelting capacity, logistics bottlenecks at ports and on rail, and strong competition from lower-cost processors in countries such as China, which import South African raw ore for downstream value-added processing.

South Africa is losing ground in the production of ferrochrome, which involves a local value-adding industrial process and local beneficiation, to China, which is the largest importer of chrome ore and the largest producer of ferrochrome, producing twice as much as South Africa.

South Africa has introduced a temporary measure to subsidise the electricity tariff, pending the development of a permanent solution. Financing the consequential revenue shortfall for Eskom has not been determined. The government has not allocated funds for this purpose in the 25/26 budget, which raises questions about the government’s intent and the risk of further cross-subsidisation by electricity consumers.

The outlook for chrome mining in South Africa

The suggested long-term solution for chrome smelters’ electricity tariff subsidies is to revamp old coal-fired power stations and allocate the generated electricity to the chrome smelters. It also includes taxing chrome ore exports and introducing export permits.

These interventions address the symptoms, not the cause. Eskom needs to address its inefficiencies and operating costs, which are among the major causes of higher electricity prices. The entity is grossly overstaffed with a complement of about 42,000, which increased by over 2000 in 2025. The World Bank estimated a 66% over staffing, poor capital allocation, and one can add unacceptable delivery lead time and cost overruns, costly procurement and mismanagement, and poor maintenance standards with excessive breakdowns compared to international standards with “cost-reflective” price increases allowed by the National Energy Regulator of South Africa (NERSA).

China has developed its own chrome smelters to reduce dependency. South Africa could reduce its dependence on ore exports to China by reinvigorating its own steel industry and improving efficiency, which is hampered by excessive electricity costs.

Going beyond trade tensions by fixing South Africa’s industrial basics

The IMF suggested that a weakened yuan, when adjusted for inflation and trade-weighted, has made Chinese exports cheaper and a bit unfair in its trade practices.

There are remedies to combat unfair trading practices, but this should not stop South Africa from urgently addressing some of the causes, such as restructuring Eskom so that it sells electricity cheaper while remaining sustainable rather than offering tariff concessions to high users at the expense of household consumers. According to Ch. Robertsons in The Time-travelling Economist, cheap electricity is one of the three essential pillars for successful economic development and that should be the focus. Without structural reform, particularly in energy pricing and industrial policy, the country will continue to export raw materials and lose out on valuable downstream beneficiation opportunities.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries Mining and quarryingSouth Africa

South Africa’s mining decline and its impact on economic growth

Contents [hide] Continued trend in the South African mining industry It is clear that South African mining production has been in decline for quite some time, a critical issue for...

BlogCountries Mining and quarryingSouth Africa

The Role of Service Activities in South Africa’s Mineral Sector

Contents [hide] The mining industry has long been a cornerstone of South Africa’s economy, with associated services being essential and critical in the value chain. The WOW report on services...

BlogCountries Mining and quarryingSouth Africa

Illegal mining – an explosive nuisance

Contents [hide] Illegal mining has grown exponentially in recent years in South Africa, as detailed in WOW’s report on the Manufacture of Explosives and pyrotechnics in South Africa . The...