Continued trend in the South African mining industry

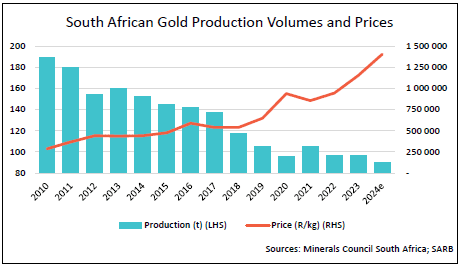

It is clear that South African mining production has been in decline for quite some time, a critical issue for the mining of precious metals in South Africa, although mineral resources are far from depleted. Who Owns Whom’s report on the mining of precious metals and minerals in South Africa indicates that precious metals exports increased by 10.1% in 2024 due to the increased price of gold, improving the performance of the mining industry despite the continued production decline.

The inevitable questions to ask are why the decline continues, and what does government need to do differently to reverse this trend? In the words attributed to Einstein, insanity is doing the same thing over and over and expecting different results.

Importance of the mining sector to South Africa

Despite the continued decline in production, the mining sector remains a vital component of the South African economic landscape. The decline has been evident in the diminishing contribution to GDP from around 20% in the 1980s to 8.3% in 2013 and 6.2% ten years later. A loss of 2.1% of South Africa’s GDP of R7.024tn in 2023 represents R147.5bn in lost economic activity, according to data from Statistics South Africa.

In 2023, South Africa’s formal employment stood at about 11.5 million. Applying the ratio of employment to GDP to the lost output, about 241,500 direct jobs never saw the light of day. The tragedy is that the loss in economic activity and value add creation can never be recovered. There is however remedy, especially given the wealth of mineral resources still in the ground, and one would imagine that the government would prioritise the revival of this important industry, a priority that on the surface seems straightforward.

Volatility of precious minerals pricing

South Africa should not delay actions to revive this industry because the recent high gold price in South Africa and globally has masked the real impact of the decline in actual production, as illustrated in the graph. In the present climate of increasing conflict between nations, the gold price is unlikely to drop a lot in value, regardless of the consistent oversupply for years.

Gold has kept its very special status as a safe haven among investors worldwide. Central banks hold trillions of dollars’ worth of gold in their safes and, according to the World Gold Council, keep adding to it. This gives gold a privileged status compared to platinum group metals (PGMs), of which South Africa has the highest reserves worldwide. Without the same standing, the PGM market in South Africa and globally is much more tied to a supply-demand market equilibrium, so these metals lag gold in pricing power.

Geopolitical shifts and associated consequences

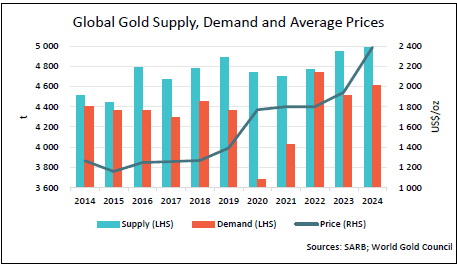

Recent political turmoil has seen a sharp upward movement in PGM prices in the last few months, impacting the PGM price outlook. These circumstances may change, but South Africa should not wait for it to happen in a world where competition can cause major damage to market shares, as shown with its gold production over time, more so than for other metals due to unwavering demand for the metal.

Safe havens change in nature over time. For example, the gold standard, with gold backing the US currency, was cancelled in 1933, while in 1971, the convertibility of US currency for gold was abolished. Today the value of the US currency is backed by the US economy, not by its gold reserves. Also, cryptocurrencies are making headway as an investment and transactional alternative, offering the advantage of convenience and flexibility that gold does not possess. The minting of gold coins for daily transactions as a medium to exchange goods is distant history.

Market forces

In recent times, developing nations have started increasing the pressure to maximise the value of their mineral and metal resources extracted by foreign companies on their land, and to advance beneficiation in their countries. South Africa has been talking about beneficiation for decades now, but has not brought this to impactful fruition. This approach has been lauded as advancing economic growth for many countries. High reserves and low extraction costs can create some leverage for a while, but with a decade-long lack of foreign direct investment in mining in South Africa, it is clear that government needs to urgently improve on its policies and create a more certain investment climate to curb the continued downward trend and the consequential loss to the economy and employment.

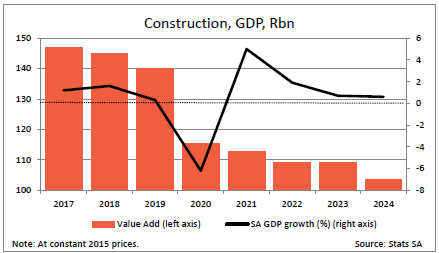

South Africa’s construction sector has been in decline for many years, with several high-profile listed companies filing for business rescue or liquidation. Large, complex infrastructure projects have followed suit as South Africa gradually lost its critical skills and, therefore, competitiveness.

This is not a great way to start a story, but the graph below from the Who Owns Whom report on the building installation industry in South Africa cannot be ignored.

How South Africa compares with international competitors

Over several years, South Africa’s spend on construction has averaged 2.5%, of GDP declining from a peak in 2017 of 4% to 2.3% by 2023. This is far below the average of 6-9% in developed countries and a range of 10-20% in developing countries

The 7.5% shortfall, equivalent to R547bn, has resulted in astronomical job losses, stalled infrastructure projects, and declining maintenance of infrastructure, and as a result, fewer services delivered to citizens.

The country is far behind international practice in terms of average spending on construction. The government revealed a significant gap in the budget that it tried to fill by increasing VAT, but it failed, while spending its tax revenue excessively on wages and social grants, leaving insufficient funds for capital projects.

However, the growing demand for renewable energy installations, mainly in real estate development and heating and air-conditioning upgrades for commercial properties, has opened new opportunities in the building installation sector. Like its international competitors, South Africa’s renewable energy drive offers growth opportunities for building installations.

What is holding the construction sector back?

The private sector has made a significant contribution to the construction sector over the last decade, spending twice as much as the public sector. Most of the private sector investment goes to residential housing, yet the shortage of housing is estimated at 2.2 million homes. The shortage is most severe in the middle-income segment, which is people earning too much for an RDP house, but not enough to qualify for a mortgage.

The supply-demand mismatch in this segment is aggravated by several important factors.

External cost escalations

The cost of construction is held back by inordinate and burdensome regulations and approvals, and the costs of bulk supply upgrades and increased regulations which are all loaded into the price of new homes, making them out of reach for many.

Cost of money

South Africa’s interest rates have been high, and some economists have argued that South Africa’s inflation is not demand-driven like, for example, the US. South Africa’s inflation rate was 3% in June, and the US was 2.9%, yet mortgage rates in the US are around 5.9% while South Africa’s home loan rates are around 10.75%.

The difference in the bond rates increases the monthly bond payment on a R500,000 home by R1,522, meaning a person would need to earn R5,075 more each month to qualify for a bond, an amount that puts homeownership out of reach for many middle-income earners.

The stability of the rand as the cornerstone of interest rate policy is a valid goal but shouldn’t be the only focus.

High interest rates attract short-term speculative investment but haven’t stopped the rand from weakening against major currencies such as the euro, pound, and yuan over the past year, and against the US dollar if a longer period is considered. Meanwhile, these high rates continue to strangle economic activity for both the private sector and government.

Benefits of a change in policy

The construction sector, which includes many budding, small, and medium enterprises that can greatly contribute to job creation, is in dire need of accessible and affordable funding, as well as reduced red tape. Supportive policies can accelerate construction activity, drive innovation and move the country out of economic stagnation with better infrastructure, improved services, more affordable housing, and higher GDP growth.

The future demand for renewable energy is going to require massive investment in South Africa. Deregulation and liberalisation of the market will create an impactful boom for the construction industry, generation plants, new and upgraded transmission lines and hopefully distribute more affordable energy to South Africans.

A comparison between the financial services industry in Botswana and other middle-income countries

The financial services sector in Botswana is similar to other middle-income countries like South Africa. According to Who Owns Whom’s report on financial services in Botswana, the industry is characterised by a mix of commercial banks, microfinance institutions, pawnshops, savings and credit co-operative organisations (SACCOs), foreign exchange bureaus, a notable presence of mobile money services and the rising fintech segment. The relatively new mobile money and fintech industries are rising fast. This is despite the country’s conservative governance and strong regulatory environment that contrasts with more liberalised peers, where innovation is faster but sometimes riskier (like Kenya or Nigeria).

The difference between commercial banks and development finance institutions (DFIs) is that the DFIs’ main activity is lending, while the commercial banks carry out both lending and transactional services. Transactional banking has regained importance due to technological advances.

Growing role of digital banking

Physical handling of cheques and transfer forms required a significant labour force to verify and correct entries, but these physical tasks have largely been replaced by technology. This has lowered costs and improved the profitability of managing and transacting for client accounts. Wells Fargo in the US was substantially fined and restricted for years, for opening unsolicited multiple accounts for clients just to multiply transaction fees. Consequently, the valuation of banks has shifted back from merchant/investment banks to more traditional, previously undervalued retail/transactional banks.

Technology has opened new avenues for transacting and competition, with new products finding a receptive market. Mobile money, a product enabled by the mobile communication infrastructure of telecoms companies, has seen significant growth. The Who Owns Whom report states that in 2024, mobile broadband subscriptions grew by 16.0% to 2.9 million from 2.5 million the previous year, and recorded a CAGR of 6.81% from 2018 (1.5 million) to 2024, facilitating increased access to financial services throughout the country.

Fintechs have sprung up to offer similar services using existing internet infrastructure. With limited infrastructure investment, fintech companies can compete on cost while providing the convenience and improvement in financial access for underserved populations, especially youth and informal sector workers.

Major players in Botswana’s financial services sector

The four largest Botswana commercial banks are all foreign-owned. The advantage of this is that the technology is transferred from parent companies, making transacting costs minimal with the support of the international banking groups. This eventually benefits the people of Botswana.

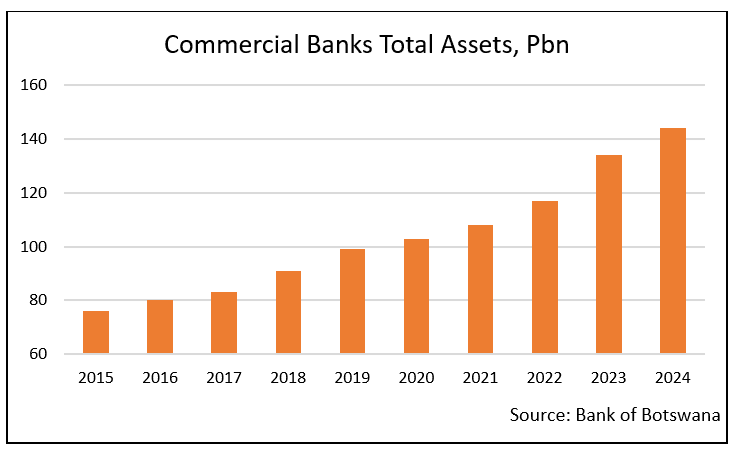

The standing, fiduciary quality and stability from conservative governance, and strong regulatory environment of major banks keeps these institutions competitive. According to the Who Owns Whom’s report, as of December 2024, commercial banks’ total assets were P144bbn (US$10.3bn), rising by 7.5% from P134bn (US$9.9bn) in 2023. The report further details the composition of the various peripheral entities in the financial industry [and can be found here].

Microlenders’ business grew by 125%, and pawnshops’ loan books by 47.6%. No reliable data appears to be available for mobile financial transactions, as they are connected to mobile subscriptions that underwent a cleanup of inactive numbers.

Botswana is still largely rural with only two towns, Gaborone and Francistown. The country’s economy, on which the banks rely, continues to show good growth. According to Who Owns Whom’s report, the real GDP growth rate was 11.9% in 2024 from 3.2% in 2023. Unfortunately, a contraction of 4% in 2025 is predicted by the IMF, due to the country’s dependence on diamonds. The cyclicality of commodities poses a risk for the country’s economy, compelling its government to find ways to diversify the economy and mitigate commodity price volatility.

The financial sector is robust and will continue to grow, although the rate of growth will be strongly influenced by the larger economic impacts caused by commodity prices until a degree of diversification is found.

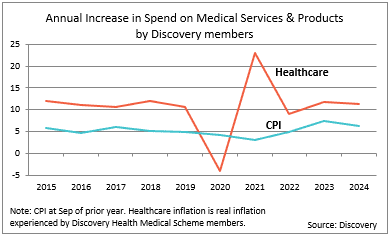

Medical aids have been in the crossfire since the NHI Bill was signed into law by President Cyril Ramaphosa in May 2024. Even without this threat, medical aids are, according to the Who Owns Whom report on medical aid funding in South Africa [found here], coming under growing strain due to the increasingly high costs of private healthcare.

It is worth looking into what is driving ever-increasing healthcare costs and the sobering view on the NHI.

Population coverage and revenue base

South Africa’s private sector medical aid industry is regarded as unsustainable as it stands, as it serves only about 15% of the population, hence the aspiration for universal coverage through the NHI. Private sector healthcare competes with the best in the world in terms of quality and efficiency of service, but it is very expensive.

In a stagnant economy with income per capita regressing, it comes as no surprise that medical aids, especially the open schemes, are seeing a decline in membership and a shift toward cheaper options in their product line-up.

The inclusion of prescribed minimum benefits (PMBs), the 25% minimum statutory solvency cushion and continued above-inflation cost increases have pushed up the average cost of medical aid premiums substantially.

Cost drivers of medical aid premiums

The cost increases are attributed to several causes such as the price pressure of medical services delivery, partly due to innovation with newer and better solutions, and the higher usage of medical services by ageing members who can still afford the high cost of medical aid cover.

The ageing membership is a result of younger households with lower salaries not being able to afford the high cost of membership, and because people with medical cover live a healthier lifestyle and therefore have a longer life expectancy. A feature of medical insurance is that the balance is maintained by healthy members subsidising unhealthy ones. An ageing membership tips this balance.

Healthcare cover options and disadvantages

These issues have created a big gap in the market which has been filled with some lower cost health insurance products that exclude minimum prescribed minimum benefits. These products do not cover major illnesses such as cancer, the treatment of which has become exceptionally expensive. For example, one advanced PET scan can cost over R50,000 and these kinds of numbers are often only a fraction of the full cost of surgical intervention and treatment, even for medical aid members, as disbursement limitations and co-payments are all too common.

Why the NHI, and is it feasible?

In principle, the government has a compelling case to introduce NHI, although the way it is conceptualised, and the proposed implementation plan, are swamped with hurdles and concerns. Most more developed countries have some form of universal healthcare, but some also struggle to fund the sector. South Africa faces two major challenges – that it does not have the financial means to support the universal healthcare system it is proposing, and, perhaps more importantly, that there is a fundamental distrust about government’s capacity to run an NHI without it going the same way as almost all parastatals that have gone to complete ruin.

Important facts about transitioning to NHI

Some statistics reveal the momentous task of transitioning to a universal health system. Currently government spends about R272bn on 85% of the population (or about 55 million people), amounting to R4,945 per person per year. Private medical aid contributions amount to approximately R260bn for an estimated 10 million beneficiaries or R26,000 per person. If a universal system is introduced then total spend of R532bn for 65 million people would equate to R8,184 per person. Supposing that private sector members’ contributions are maintained, the average available to them would drop from R26,000 to R8,184. The contention is that private sector medical providers’ cost structures cannot be reduced by such an amount to provide the same level of service. The 15% of the population on medical aid do not have the means to fund the shortfall, nor does the government have the funds to increase its health budget by about R1.1tn.

Ideal way forward

A more effective long-term transition model is needed, one that would largely maintain private sector participation and incentives while crafting a feasible roadmap toward universal access to quality health care and a thriving industry.