Growth in illicit trade and the impact of sin taxes in the South African liquor industry

“In vino veritas” (in wine there is truth). The liquor industry in South Africa reveals a complex and evolving industry that is thriving despite high taxation, a complicated regulatory framework, economic pressure and an increase in illicit products.

The increasing trade of illicit alcohol in South Africa

This industry is one of the most taxed, alongside cigarettes, sugar, and speeding. All of them are victims of the exploited inherent contradiction. They are all high-income taxpayers, taxed by a government under the guise of lowering consumption and putting the money to good use. The question would be, has the sin tax policy reduced consumption over the years, and is it the best tool to achieve the noble objective of better health?

There are, of course, limits to this ambivalent strategy. This was clearly illustrated in how the draconian measures against alcohol and tobacco distribution during the COVID lockdown unintentionally set in motion the growth of illicit trade in both products, which has become an entrenched, permanent and growing feature of South Africa’s economy today.

Sin taxes, pricing pressure and increased alternatives

Over the years, the (above board) volumes on which government can raise taxes show growth, but a significant amount has shifted to the informal or illicit industry. These missing volumes are hidden but significant. The worst case of tobacco industry decline we have seen is the demise of the biggest local manufacturer (BAT), which closed its doors in South Africa, resulting in economic and direct loss of employment of several hundred. Alcohol consumption still increases every year and by itself does not yet raise alarming red flags; tax revenue could have seen much bigger numbers were it not for illicit alcohol sales, which have become significant.

The hurdle for government has become the level of taxes included in the end products. The annual increases have not been excessive as with Eskom tariffs, but in a stagnant economy where the average income to GDP has declined since 2021, when it stood at $6,924 compared to $6,667 in 2025, cost increases, especially those caused by administered prices, hurt, and the items bought from discretionary income suffer the most. This has provided an incentive for illicit trading and further boosted the traditional manufacture of specific alcohol products such as “Thothotho”, which was re-ignited during the Covid-19 lockdown period.

Price pressures resulting in consumers buying down

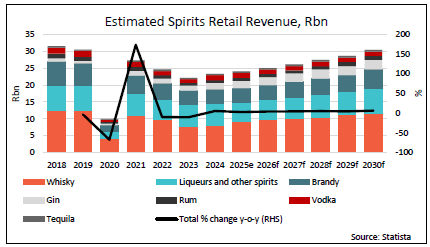

The pulling power of alcohol is strong. The Who Owns Whom report on The Liquor Industry in South Africa indicates that there is a clear trend to down-buying, though. Premium brands with large price differences, mainly in the spirits sector, have been affected the most. As affordability declines, consumers move to cheaper options. Over the years, there has, for example, been a clear shift from more expensive whisky to cheaper gin.

The Who Owns Whom report indicates that from 2015 to 2024, gin market share grew from 5.1% to 25.6%, a CAGR of 20.2%, while whisky shrank from 33% to 19%, a CAGR of minus 3.3%, with a bias of bigger declines in the more recent years.

Beer, taking centre stage in local production of alcohol

In terms of litres consumed, beer outpaced everything else with 3.7 billion litres in 2024 (73.1% of all litres consumed), up 4.4% from the previous year. And the beauty about the beer industry is that the whole supply chain is 90%+ made up of local inputs! This makes it worth looking at innovative and progressive regulation and tax regimes that are holistic in approach.

Another segment worth keeping an eye on is the Ready To Drink (RTD) beverage segment, which saw phenomenal growth, albeit from a low base in terms of litres of alcohol consumed. It far outpaced other spirits, growing by 162.2% from 2004 to 2024, while other spirits grew by 79.1%.

Balancing regulation and economic growth

Increased health risks of unregulated products, in the context of economic progress, require policies and measures that support the industry while carefully considering unintentional incentives for illicit trade that could hurt tax revenue.

Industry experts have indicated that a narrow focus on sin taxes to fill budget gaps, without considering the health risks of non-compliant products, can negatively impact economic activity and increase the burden of disease on the government. Regulation should combine moderate, fair taxation, bylaw enforcement to restrict illicit trade, and public health measures such as responsible consumption campaigns and strict drink-driving laws, that together protect economic value while reducing harm.

The size of the illicit market is massive enough to warrant attention and measures to reduce it. This will increase tax revenue as people, grudgingly or not, revert to official outlets with legitimate products.

Judicious choices in managing the alcoholic beverages sector will benefit everyone, and good wine will remain affordable and be consumed. In vino veritas!

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries ManufacturingManufacturingMozambique

How the tobacco industry in Mozambique evolved from cash crop to a strategic commodity

Kenya's telecom sector is evolving fast. Learn how M-Pesa, regulatory reform, and mobile penetration are driving digital growth and financial inclusion across the country.