The resilience of the South African construction industry despite structural constraints

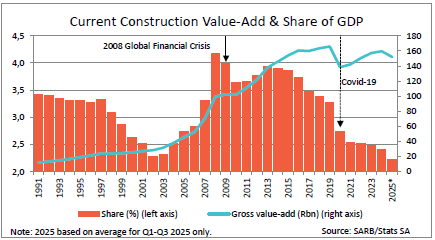

The South African construction industry went through a difficult period marked by company failures, stalled infrastructure projects, weak investments, and an uncertain policy regime. According to the Who Owns Whom report on the construction industry in South Africa, the industry’s contribution to the economy has declined for eight straight years and continued to decline in 2025, despite some improvement in civil building confidence towards the end of the year. Its contribution to the economy in 2024 was 33.6% lower than in 2016. As 2026 unfolds, there seems to be renewed optimism, driven largely by private-sector activity and the growing role of smaller contractors.

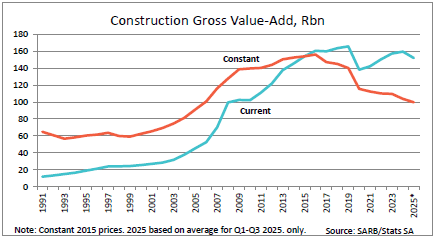

The industry’s persistent decline led to several large and listed construction companies collapsing or downsizing, with Basil Read, Group Five and Murray & Roberts being the most well-known casualties. Overall, it manifested as a drop in value-add and in its share of GDP, as illustrated here.

Private sector resilience and a glimmer of hope

Only in the last quarter of 2025 and the beginning of 2026 was there a glimmer of optimism, indicating that things are turning around. Confidence levels rose cautiously, although this was before the outbreak of the war in Iran, which is creating uncertainty around global energy supply and will have ripple effects worldwide, including in South Africa.

Infrastructure investment is generally dominated by governments, with the public sector accounting for more than 70% of funding. However, in South Africa, the situation is almost reversed; According to the Government Technical advisory Council, the structural split in South Africa is 71.4% by the private sector while the government including SOEs contributes approximately 28.6%. The consequence is visible in the country’s gross fixed capital formation (GFCF) levels, which are significantly below the 20% to 30% levels in other developing countries.

Capital Investment Comparison: South Africa vs Emerging Market Peers

Gross Fixed Capital Formation (% of GDP)

| Country | Gross Fixed Capital Formation (% of GDP) | Real GDP Growth (%) | Interpretation |

| South Africa | 15% | 0.6% | Low investment and weak growth |

| Brazil | 18–19% | 3.4% | Moderate investment, modest growth |

| Mexico | 22–23% | 1.4–1.5% | Average investment, slow growth |

| Indonesia | 30–31% | 5.0% | Strong infrastructure investment supporting growth |

| India | 33–34% | 6.5% | High investment driving rapid expansion |

| China | 42–44% | ~5.0% | Very high investment-led growth |

Source: World Bank: World Development Indicators – Gross Fixed Capital Formation (% of GDP).

South Africa’s infrastructure investment of 15% is the lowest l among developing countries listed in the table above, which is not surprising given the associated economic growth. The need to improve this score is undeniable, with a strong correlation between a high GFCF and high economic growth.

Sector challenges and the rise of the SME segment

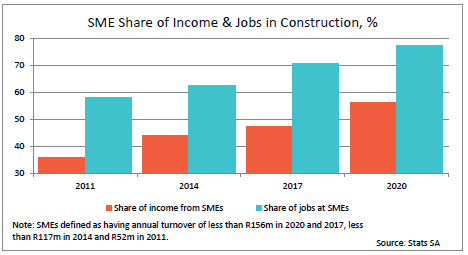

The resilience of the private sector is seen in the increased and more diversified contribution of SMEs to sector activity.

The SME share of income and jobs has steadily risen over the last four years.

Larger companies have sourced a growing portion of their work and order books beyond South Africa’s borders, with the highest scorer being Aveng, generating more than 90% of its R31bn revenue outside South Africa in 2025.

Government has launched several initiatives to reinvigorate the sector, including Infrastructure South Africa (ISA), set up by the presidency in 2020, which is yet to deliver the scale of investment the industry was hoping for, and its impact is not yet apparent. The stark reality is that South Africa has run up a huge debt relative to its slow-growing GDP, severely limiting its capacity to allocate meaningful funds to increase public sector investment.

The well-known economy-wide problems such as crime, corruption, and construction mafias cause untold damage to the sector, including delays and abandoned or incomplete projects.

Outlook for 2026 and beyond

The outlook for 2026 in terms of industry sentiment is the most positive in years, although global uncertainty may slow the recovery. The path to full recovery will be long and hard, especially since it will take several years to reset and restructure government finances to free up more funds for infrastructure investment. In the words of Chinese philosopher Lao Tzu, a journey of 1,000 miles starts with the first step. The recovery may be slow, but the industry’s resilience promises to be an essential pillar to future growth.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries ConstructionSouth Africa

The boom and bottleneck in South Africa’s building installation industry

Contents [hide] South Africa’s construction sector has been in decline for many years, with several high-profile listed companies filing for business rescue or liquidation. Large, complex infrastructure projects have followed...

BlogCountries ConstructionSouth Africa

The Impact of Infrastructure Development Challenges in South Africa

Contents [hide] The importance of capital formation for infrastructure development Infrastructure development has many elements including fixed capital formation, a statistical term for just about everything that constitutes investment in...

BlogCountries ConstructionSouth Africa

Nanotechnology in the Paints and Coatings Industry

Contents [hide] What is Nanotechnology? Nanotechnology is one of those many new technology buzzwords that are accepted in daily discourse but not very well understood as the magnitude is outside...