South Africa’s air transport and aviation’s re-mergence, its struggles and opportunities.

The Who Owns Whom report on air transport and aviation ground-handling services in South Africa highlights the paradox of how a powerful economic enabler that drives tourism, trade, and investment continues to struggle financially. This is a low-profit, high-impact industry with thin airline margins, high fuel and leasing costs and a high level of regulation.

Two shocks that disrupted the industry

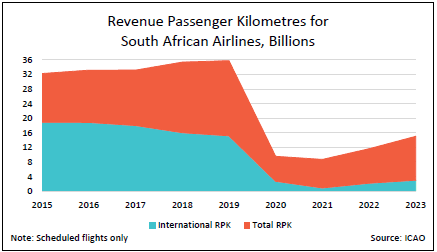

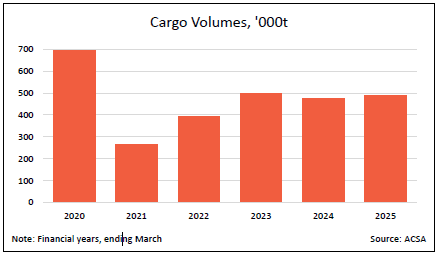

The industry experienced a long period of major disruptions, resulting in a severe contraction, with revenues affected and not fully recovered. The passenger and cargo volumes indicated in the graphs here tell the story.

The first upheaval occurred when South African Airways (SAA) entered business rescue, a process that was widely perceived as costly and unsatisfactory. The result was a significantly slimmed-down airline that also lost many overseas landing rights. The COVID lockdowns and travel restrictions were the other major upheaval, with a dramatic impact evident in 2021 cargo volumes.

SAA’s lean restart: a creative destruction in action?

If one applies Schumpeter’s concept of creative destruction, SAA emerges as a good case study. The airline, operating a fleet of 49 aircraft with huge losses for several years, entered business rescue and resumed business with just six aircraft in 2021. It adopted a lean strategy focused on cost-cutting and sustainability, unlike the most profitable airlines, such as Emirates, which operate large, modern fleets capable of deploying on high-yield routes.

SAA has since managed to increase its fleet to around 19 aircraft in operation and six on order in 2025. The average age of its fleet is around 13, which compares favourably with the world average of 14.8 and certainly to the African continent average of 17-20 years.

Low profits, high economic power

Despite SAA being late with its annual financials and the Auditor-General’s audit opinion not being included in the financial statements, SAA is conveying that profitability is improving, with a declared profit in 2024/25 as opposed to a loss in the previous year. SAA also has expansion plans with several international destinations lined up.

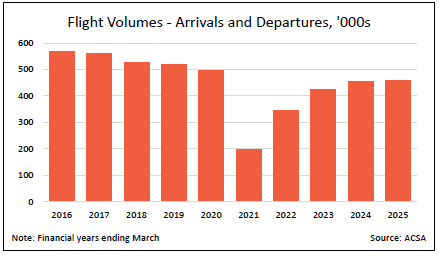

The broader transport and aviation handling services, however, have not improved at the expected rate since the pandemic.

Flight volumes, as shown here, have not sufficiently recovered to pre-pandemic levels.

The lack of sufficient recovery extends to the wider aviation sector. Stats SA’s latest large survey report on the air transport industry (excluding airports, air navigation and ground-handling services) recorded revenue of R45.1bn in 2023, down from R64.7bn in 2019 when the previous large survey was completed. While airlines struggle to turn a profit, their reduced capacity has immediate economic consequences for connectivity and pricing.

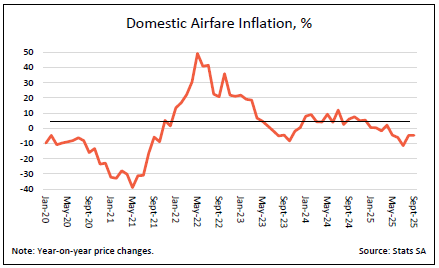

The sudden disappearance of SAA as the dominant airline created a period of seat shortages, with a few local airlines taking advantage of it by operating local flights at much higher prices. The price increases were so excessive that the Competition Commission had to issue a warning against price gouging.

The proverbial “chickens come home to roost” played out, and price decreases followed as supply was picking up on demand.

Why has recovery has been slower than expected

The Who Owns Whom report further indicated that while annual passenger growth has been strong since the pandemic, it slowed between 2024 and 2025. A 10% decrease from the high prices was insufficient to offset the previous 40%-plus increases. Domestic flight volumes (arrivals and departures) declined to 240,741 in the year to March 2025 from 245,470 in 2024 after years of persistent recovery since 2020. ACSA data also shows a drop in the number of cargo flights to and from ACSA airports from 16,000 in 2021 (above the 11,000 in 2020) to 8,000 in 2025.

The industry must be wary of the deterioration in the overall service standards and levels.

Air Traffic and Navigation Services’ (ATNS) failure to review and approve new procedures in time from 2023 meant existing procedures became a safety risk and their use was suspended. The result was that pilots had to approach affected runways without instruments. A March 2025 Daily Maverick article reported that one airline experienced 3,892 delayed flights, 77 cancellations, and 12 diversions between July and November 2024, costing it 63 days of flying time, according to ATNS.

What matters now

The air transport, aviation, and ground handling industries have significant growth potential that warrants attention. The intended acquisition by Harith of South Africa’s largest airline, FlySafair, is a positive move that can reposition South Africa’s air transport and aviation industry. As stated in a TimesLive article dated 10 February 2026, the proposed deal fulfils Harith’s long-held ambition of owning an airline, after its deal to acquire a majority stake in SAA collapsed in 2024 when the private equity firm walked away from the transaction after it was caught up in a political storm. According to media reports, FlySafair has grown to be a market-leading low-cost carrier since its establishment in 2014. It holds 67% of all domestic seat capacity with a fleet of 39 B737 aircraft. The airline has carried more than 54 million passengers at reduced fares on common routes.

Aviation analyst Phuthego Mojapele cautioned that whilst the transaction could prove a sound investment, it would be important for Harith’s shareholders, including the Public Investment Corporation (PIC), to be assured that thorough due diligence had been conducted.

Further opportunities after COVID and the collapse of SAA lie in the rebuilding of the local aviation industry to its former glory. This entails investing in leasing aircraft, logistics platforms, cargo hub positioning, maintenance, repair, and overhaul capabilities, airport-linked logistics zones, ground-handling efficiency, and air navigation resilience.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

Blog South Africa

Beyond the grave, and the evolution of culture in the funeral services industry in South Africa

Contents [hide] Funeral services and related industries have undergone a gradual transformation since the advent of democracy in 1994 from a community-based, culturally driven sector into a complex, multi-billion-rand industry...

BlogCountries Human health and social work activitiesSouth Africa

South Africa’s Healthcare Challenges and the Future of Universal Health Coverage

Contents [hide] Healthcare is a vital cog in any economy. When the nation’s workforce is healthy, there is more economic activity, businesses do well with less absenteeism and highly productive...

BlogCountries MozambiqueSouth Africa

Petroleum in Mozambique: powering growth and energy security

Contents [hide] Clean energy and environmental concerns are taking the spotlight globally, with the move to electric vehicles taking centre stage. It is reportedly near the end for petroleum as...