The starch industry – vast prospects in its versatility

South Africa’s starch production landscape

The older generation might remember starch being used to stiffen shirt collars, without realising that it is not just used in laundry but also an (edible) unsung hero, a powerhouse driving industries and livelihoods. Starch is found in maize, potatoes, cassava, rice and wheat, among others and supports agricultural jobs and fuels innovation. Its multiple uses, in original or modified form, are derived from its qualities as a thickener, binder, filler in food, a carrier, humectant, and gelling and moulding agent.

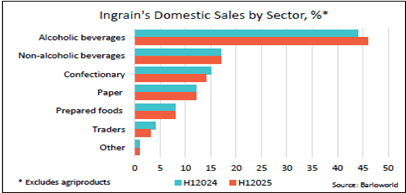

In South Africa, Ingrain, formerly a division of Tongaat Hulett, is the largest producer of starch, which is mainly derived from maize. According to the Who Owns Whom report on The Starch Industry in South Africa including Sorbitol, Ingrain processes around 660,000t to 700,000t of maize into starch, glucose and various agriproducts annually, while the combined output of smaller local starch producers is estimated at between 12,000t to 30,000t annually. The latter represents a mere ≈ 4% of the total South African production. Wet milling of 1 t of maize would roughly yield 60-65% starch, along with fibre, gluten, and germ.

This makes Ingrain’s sales a good reflection of various uses of starch in the South African market. It is evident that in South Africa, starch has not yet found avenues for many of the potential applications in the industry segments listed above, highlighting prospects across several industries.

Import pressures and industry challenges

Starch processing is not spared the ongoing challenges in the manufacturing sector, such as rising electricity costs, ageing equipment, and headwinds from cheap imports. South Africa imported 98,205t of starch in 2025, an increase of 15.5% from 85,035t in 2024, while exports fell by 15.9% to 41,227t in 2025 from 49,003t in 2024, this while domestic starch supply increased by only 1.9% to around 496,000t. These trends show increasing reliance on imports and weakening export competitiveness.

Comparison to global players

Compared to the US, where about 15% of corn is used for starch production, South Africa uses only about 4% of its annual maize production for starch. The US also has a deeper application of starch into industrial applications, with a large component going into the production of ethanol, an application which is basically not yet utilised in South Africa.

Growth opportunities through industrial strategy

There is potential for growth of the starch production market in South Africa if only the hurdle of the capital-intensive process and high operational costs, driven mainly by the cost of electricity and logistics support for exports, could be more efficiently mitigated. Smaller operators might find it difficult to fund new installations to match international competition, while large existing manufacturing businesses like Ingrain, benefit from the historical averaging of the capital investment, but in the long term will face the mounting problem of outdated, less efficient and more maintenance prone equipment if they do not follow sound practices of continuous investment in renewal – this amounts to living on borrowed time.

Driving demand and industrial growth, leading to economic growth

South Africa can avoid another Arcelor Mittal by improving the business environment and lowering electricity costs, which currently absorb funds that would otherwise be directed to innovation and new investments. Improving logistical support can contribute to the country’s export competitiveness.

Starch production holds significant opportunities, particularly for modified starches, across a wide range of industrial applications and offers higher value-adding margins, supporting the feasibility of new ventures. On the input side, the ARC’s (Agricultural Research Council) pilot to produce cassava, a more drought-resistant crop with high starch content, is yet to be commercialised. Producing price-competitive, high-quality starch variants can drive demand, increase local demand at the expense of imports, and expand export markets, earning much-desired foreign currency. This would amount to job creation, economic development and higher GDP growth.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries ManufacturingManufacturingMozambique

How the tobacco industry in Mozambique evolved from cash crop to a strategic commodity

The tobacco industry in Mozambique has always been an integral part of the country's economic activity, serving as a subsistence crop bartered among its communities.

Blog ManufacturingSouth Africa

The not-so-sweet future of South Africa’s Sugar Manufacturing Industry

Contents [hide] On the one hand, the sugar industry is fighting against the tide, with consumption of sugar products decreasing by about 4 to 5% a year in most countries,...

Blog Manufacturing

The power of the mill: Food security and the evolution of South Africa’s grain sector

Contents [hide] Flour and grain mill products are central to food security and the backbone of the agro-processing ecosystem. Grains are a critical input for baking, brewing, animal feed, and...