The power of the mill: Food security and the evolution of South Africa’s grain sector

Flour and grain mill products are central to food security and the backbone of the agro-processing ecosystem. Grains are a critical input for baking, brewing, animal feed, and processed foods that sustain both urban and rural economies. Global consumption patterns differ: In South Africa, maize is the most important basic food, rice is the staple in Asia, rice and maize in the US and wheat in Europe. Rice is the most important staple globally, followed by wheat and then maize.

The South African milling industry has fundamentally evolved with deregulation, technological advancements and changing consumer preferences. The rise of informal and small-scale millers has restructured this sector, which was once dominated by large, vertically integrated players.

The word mill refers to wheat and maize mills. Maize mills are relatively more complex, performing more tasks than just grinding and include degerminators (to remove germ and bran), roller mills (to break and grind the endosperm), plansifters, hammer mills (in some systems) and polishers (depending on product)

Technological changes and consumption trends in the milling industry

The Who Owns Whom report on the Manufacture of Flour and Grain Mill Products in South Africa [found here] notes that the trend of larger mills losing market share to smaller grain millers was enabled by technological improvements that made smaller mills more accessible and affordable for smaller players. The flexibility and agility of smaller players, combined with shorter turnaround times and follow-through on specific demands, are making it more difficult for larger mills to remain competitive. The growth of the informal sector, which has lower overheads, is the main reason for this fundamental shift toward smaller-scale supply to meet varying demands. Localisation and changing consumer preferences for cheaper and/or healthier gluten-free or culturally relevant grains, rather than “super” maize, underscore the trend.

These are welcome developments for the country, as they contribute to the decentralisation of economic activity and to increased competitiveness among the major players who continue to fight for market share to maintain a growth trajectory.

Capacity of the South African milling industry

The fragmentation of the milling industry has made it difficult to measure the extent to which annual installed capacity is utilised. Current estimates suggest capacity utilisation of about 80% of the 5Mt annual capacity, or about 3.8Mt. The capacity utilisation rate is similar among wheat millers, who operate in an industry that imports significant quantities of raw wheat for local milling, with 40-60% of wheat consumption met by imports.

To protect the local wheat crop, South Africa’s wheat tariff increased to R851.50/t from 11 July 2025 from R549.50/t previously. The tariff kicks in when international wheat prices fall below a reference price, which is currently US$279/t (following a request from Grain SA and others, the International Trade Administration Commission (ITAC) tabled a new reference price of US$289/t in April 2025 for comment, which was still under consideration as of publication of this report). The protection mechanism can only achieve the aim of increased local production if it adapts to market conditions in good time.

Climatic conditions and key challenges in the milling industry

Climatic conditions in South Africa do not favour competitive wheat farming, affecting grain availability, prices, quality, and operating stability. The industry is also affected by heavy subsidisation from exporting countries, with importation likely to remain a permanent feature, even though wheat consumption is lower than that of maize in South Africa.

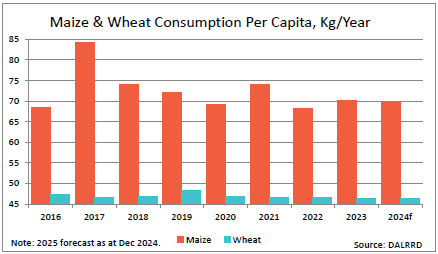

Production swings also lead to periods of underutilised milling capacity, increasing the risk for millers, particularly for smaller players. In fact, according to the Who Owns Who report, per capita wheat consumption has edged even lower over the last decade, likely due to increased consumption of maize products compared to wheat.

The tariff protection measure for wheat farmers does not seem to be working too well in practice, due to time delays and the slow decision-making process of the operation of the mechanism, which significantly defeats the purpose of promoting and encouraging the farming of wheat. All these challenges are exacerbated by high electricity costs and challenging logistics support.

The logistics challenges, with Transnet reporting that grain volumes railed declined by 12.7% to 390,000t in the year to end-March 2025 from 450,000t in 2024, do not contribute to growing the local industry. These transport challenges and the expensive and unreliable power supply have led to rising input costs.

Way forward for the South African milling industry

For the milling industry to remain sustainable in the long term, it will have to effectively adapt to new technologies, invest in renewable energy solutions and improved storage, and integrate farmers into a pathway that improves efficiency and resilience. Other innovations such as crop rotation practices and increasing the production of culturally relevant and gluten-free grain products, must be implemented to support the expansion of localised milling services. Reliable infrastructure, responsive policy, and climate-smart agricultural practices will boost South Africa’s flour and grain milling sector and contribute to a competitive, inclusive, and resilient industry that ensures food security.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

Blog ManufacturingSouth Africa

The not-so-sweet future of South Africa’s Sugar Manufacturing Industry

Contents [hide] On the one hand, the sugar industry is fighting against the tide, with consumption of sugar products decreasing by about 4 to 5% a year in most countries,...

BlogCountries ManufacturingSouth Africa

South Africa’s Plastic Manufacturing Industry: Innovation, sustainability and investment opportunities

Contents [hide] Plastic is a versatile, cost-effective, and useful product with a wide array of applications in almost every industry, from food to transportation, packaging, and manufacturing. Technological innovations and...

BlogCountries ManufacturingSouth Africa

Manufacture of basic chemicals in South Africa, a strategic pillar for industrial development

Contents [hide] Basic chemicals, or commodity chemicals, are fundamental building blocks used for making complex products. They are typically produced in large volumes, used as raw materials, and are generally...