Why the strong South African retirement funding industry still leaves most unprepared

Contents [hide]

South Africans face mounting financial pressures and that does not assist the current challenge of the low household savings rate of 1.2% of disposable income, according to the Wall Street Financial Services website. This is reported against a backdrop of only about 6% of citizens saving enough for a comfortable retirement.

The Who Owns Whom report on retirement funding in South Africa highlights an interesting

phenomenon. South Africa’s pension assets were equivalent to 83.2% of GDP at the end of 2023, well above the global average of 33.9% and the Organisation for Economic Cooperation and Development (OECD) average of 49.8%. While this suggests a deep pool of retirement savings, coverage in South Africa remains limited, with many informal and lower-income workers remaining outside the system and underprepared for old age. This large asset pool does not translate into adequate retirement for the majority.

The Two-pot retirement system explained

The latest development in the sector was the introduction of the Two-Pot system, which, in reality, is a three-pot system that splits retirement savings into three components:

| Pot | Description |

|---|---|

| Retirement pot | Cannot be touched until retirement |

| Savings pot | Accessible once a year for emergencies |

| Vested component | Old savings not affected by the change |

The government introduced this system, citing relief for struggling citizens amid rising costs of living and sluggish economic growth. On the face of it, the two-pot system looks like a noble idea until one scratches the surface. The accessible portion is taxed at the marginal income tax rate and is, de facto, removed from pension savings.

Conservative actuarial principles with shifting liability

The South African retirement funding industry is based on the conservative actuarial principle that income-generating assets must accumulate to fund future retirement obligations. However, the private sector has simplified future obligations, shifting from defined benefit, where the employer remains responsible for the pension based on an individual’s employment earnings, to defined contribution, where the amount accumulated via contributions becomes, on retirement, the final amount available for one’s pension.

The essential difference is that, with a defined contribution, the employer’s liability ends with a person’s retirement. The public service, however, has till now remained with the defined benefit, which, if assets do not cover pension obligations, has recourse to taxpayers to fill the gap.

How South Africa differs from the developed countries

As mentioned, the industry applies conservative principles that differ markedly from those of

Western nations that operate a pay-as-you-go (PAYG) system, in which current social security

contributors fund current state pensions, with only a small fraction of private pensions actuarially

funded. This explains South Africa’s 83.2 pension assets-to-GDP ratio, which towers over the global average of 33.9%. High assets are not necessarily a sign of a successful and satisfactory pension system but only indicate a different funding model.

The need to interpret these percentages is starkly relevant when Who Owns Whom reports that only about 6% of South Africans are on track for a comfortable retirement, compared with 40-60% in the OECD, with some countries reaching 70-80% (Netherlands and Denmark).

Three fundamental problems beyond the pension industry

The apparent problem for South Africa of its woefully inadequate pension provision while aiming for

a better pension provision, lies outside the pensions funding arena.

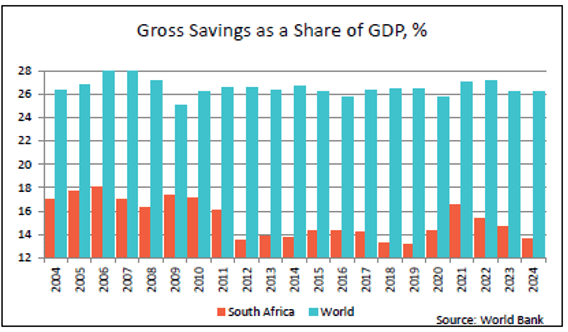

Firstly, South Africa is plagued by persistently high unemployment of about 43,7%. Most of the unemployed will rely on the government’s subsidised old age grant, not a privately funded pension, due to low wage levels limiting individual savings towards a pension. The immense disparity in saving levels is illustrated here.

The apparent problem for South Africa of its woefully inadequate pension provision while aiming for a better pension provision, lies outside the pensions funding arena.

Firstly, South Africa is plagued by persistently high unemployment of about 43,7%. Most of the unemployed will rely on the government’s subsidised old age grant, not a privately funded pension, due to low wage levels limiting individual savings towards a pension. The immense disparity in saving levels is illustrated here.

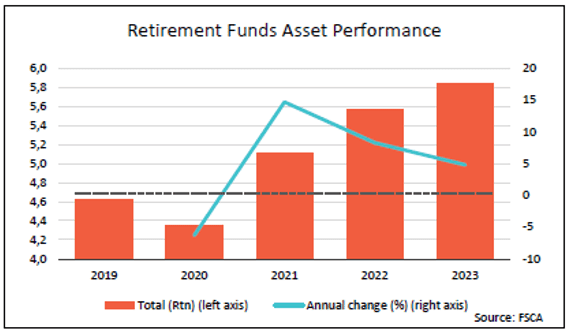

Secondly, South Africa has experienced decades of stagnant economic growth and many years of low wages, meaning that companies struggle to afford pension arrangements, and of those that do, many fall behind on contributions, dragging down asset returns, as shown here.

Thirdly, even some SOEs and several municipalities fail to make pension contributions due to negligence and maladministration.

Consequence of an overstretched old age grant

As a result of the above, government ends up with an overextended old-age pension obligation, crowding out other, more productive budget allocations for education, health and infrastructure development, to name a few.

Surveys by FNB, Old Mutual and PwC all point to the same outcome: a very high percentage of those with a privately funded pension use their withdrawals from the two-pot system for current expenses and debt, while a small fraction invests in productive assets.

The need was evident. The Who Owns Whom report states that two-pot system withdrawals totalling R79.3bn, with a tax liability of R21.4bn, were approved between September 2024 and the end of February 2026. More than 5.6 million people applied for tax directives for these withdrawals.

Against this backdrop and given the magnitude of the withdrawals, even though people know that early withdrawals are taxed at marginal rates and do not enjoy the tax benefits of withdrawals at retirement, one cannot but be sceptical about industry experts’ anticipation that the two-pot system will strengthen the long-term preservation of retirement savings, especially as additional permitted withdrawals resume extensively in every new tax year.

A sound system hamstrung by broader failures

South Africa has a well-capitalised, conservatively managed retirement funding industry, but a stagnant economy, high unemployment and low wages mean that most citizens will not benefit from sufficient long-term accumulation of contributions. Unless the government addresses the wider economic challenges, achieving comfortable pensions for the majority will remain an illusion. All South Africans who are still in employment will have to make every effort to increase their pension contributions to offset the effects of early withdrawals.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries South AfricaTransportation & Logistics

The South African Courier, Express and Parcel Services: A shining star of the e-commerce industry

E-commerce growth, mobile technology and changing buying patterns have powered South Africa’s Courier, Express and Parcel (CEP) Services industry turning it into a critical link in the digital economy.

BlogCountries Automotive & PartsSouth Africa

Beyond assembly lines of the South African motor industry, supply chain resilience and shifts in the industry

Manufacturers are no longer grappling with how many units they need to produce, but with how they will survive the volatile, low-carbon, and digitally driven future, whilst remaining competitive.

BlogCountries ManufacturingManufacturingMozambique

How the tobacco industry in Mozambique evolved from cash crop to a strategic commodity

The tobacco industry in Mozambique has always been an integral part of the country's economic activity, serving as a subsistence crop bartered among its communities.