South Africa’s manganese industry, powering the global energy transition

Contents [hide]

One of South Africa’s competitive advantages

Manganese is no longer only indispensable for the steel industry, but has taken centre stage in the global energy production, positioning the mineral as a strategic resource for economic growth. South Africa currently has the largest known deposits in the world. Manganese is part of the group of metals and minerals in demand from new technologies deployed in the production of high-demand products, prominently batteries, a critical component in the move towards electric vehicles.

Sitting on the world’s largest deposits of an in-demand commodity can be seen as an invincible advantage for South Africa. Forward-looking strategists recognise that sustained competitiveness requires intentional long-term industrial plans and continuous technological innovation to mitigate and evolve beyond temporary monopolistic advantages.

A good example lies in how, on the opposite side, the USA reversed decades of dependence on oil imports and legislation prohibiting the export of the same, to become a fully independent oil producer. Today, the USA produces more oil than it consumes. Continued exploration, shale-oil discovery, and technological innovation combined to produce this result. Markets reward those who stay abreast of developments rather than those who rely on what comes naturally.

Manganese demand trends

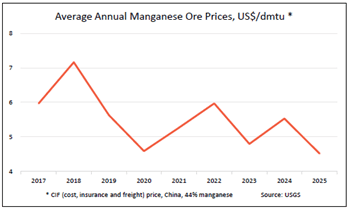

While manganese has become more popular as part of the group of new minerals and metals in demand for eco-friendly, subsidised technologies like electric vehicle batteries, for now, its main market, by and large, remains the steel industry. According to the Who Owns Whom report on the mining of manganese in South Africa, 96% of manganese supply goes to the steel industry, and so far, only 3% to battery uses, with the remaining 1% to agriculture for fertiliser and animal feed. Also inferred from the information in the Who Owns Whom report is that the steel industry is a very mature market with modest growth rates. This is reflected in the manganese pricing, which has not gone through the roof as gold did, for instance.

Battery market risks and mineral substitution threats

While battery demand is on the increase, competing production alternatives do exist, and should the cost of certain components become prohibitive, alternatives may become more attractive and impact the growth of manganese-based battery production. The black swan event, like the US-Iran war, plays in the hands of electric vehicles, boosting demand for batteries.

Manganese mining in South Africa remains advantageous given its dual application in a mature but big steel-making industry and the new applications supporting growth in demand.

The beneficiation gap in South Africa’s mining sector

One hindrance to the South African manganese industry is its local beneficiation capacity, exacerbated by high energy costs and infrastructure bottlenecks. The high cost of electricity has also resulted in the closure of several ferromanganese smelters. The Who Owns Whom report indicates that in 2020, Samancor Manganese put its Gauteng Metalloys ferromanganese smelter on care and maintenance due to loadshedding, and in August 2025, Assmang closed the Cato Ridge Works ferromanganese smelter in KwaZulu-Natal, largely due to high electricity prices that negatively impacted its profitability and globally competitiveness.

As a result, South Africa’s manganese alloy output has declined from around 800,000t per year in the previous two decades to less than 200,000t currently. A similar occurrence happened in the ferrochrome industry.

Eskom’s pricing and the need for reform

The struggling ferrochrome production prompted Eskom to implement a temporary, ringfenced electricity cost relief for two ferrochrome smelter companies (Samancor and Glencore-Merafe). This focused ringfenced subsidy is not a long-term solution as it disadvantages all other energy-intensive industries, including manganese, a strategic mineral in South Africa.

To elaborate, one can argue that the ringfenced solution was implemented too late in the day, just before the total demise, when several smelters were already put into care and maintenance. Why is there a need for other electricity-intensive users such as ferromanganese, which already lost 600,000t of production, aluminium and others to first reach a similar bear-final stage before more reasonable electricity tariffs are extended? An issue to be addressed urgently.

South Africa vs China electricity costs

According to the Serrari Markets Indexes, the current cost curve of electricity for ferrochrome and ferromanganese indicates that the latter uses slightly less power per ton produced.

In numerical terms, the electricity cost in China ranges between R0.50 and R0.73/kWh, in South Africa, before the recent concession to two ferrochrome smelters, the cost was between R1.30 and R2.00+/kWh, which makes up about 40% of production cost.

Eskom’s R0.87 but subsequently R0.62 interim agreement is still above China’s electricity cost. For the steel industry as a whole in South Africa to be competitive, the cost would have to be about R0.62 for all energy-intensive users as a long-term solution to capture the value added from local ore deposits.

Industrial transformation for Eskom

The impact of high electricity costs for South Africa’s smelters runs into billions, and for Eskom to make a difference, it would have to follow the World Bank recommendation to remove redundant staff, which by itself could save billions.

Understanding a problem is half the solution; the other half is apparently political will. Needless to underscore that the loss of employment at Eskom by removing redundant staff would be more than offset by the gain of employment in the smelter industry if smelters are reopened, and at market-related rates, making it sustainable without the need for government intervention or subsidies.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries MiningSouth Africa

Copper Re-emerges as a Strategic Mineral for South Africa

As countries transition toward renewable energy decarbonisation, they are shifting investment towards modern electricity infrastructure for electric vehicles (EVs), which require energy storage, and towards clean energy technologies.

BlogCountries MiningNamibia

Mining in Namibia, still the cornerstone and a powerhouse in the global mineral race.

The country might be small in economic terms, but it is certainly punching above its weight compared to other African countries endowed with more resources.