The financial services sector in South Africa stretches from the South African Reserve Bank to micro lenders, cooperative banks, stokvels and loyalty programmes that have become popular for customer engagement and enhancement of services. This is articulated in the WOW report on the banking industry in South Africa.

Banking, as experienced or aspired to by citizens, has been mainly carried out by the five largest banks – Standard Bank, First National Bank (FNB), Nedbank, Absa, and Investec, which collectively held 89.5% of total banking sector assets at end-March 2023, and increasingly by newer entities manifesting as simplified low-cost banking such as Capitec, digital banks such as TymeBank and Bank Zero, and pure fintech companies, with some of them backed by large corporates such as Vodacom.

Commercial banks present and future

Commercial banks essentially have two legs, retail and corporate, with the latter including business banking, advisory services, trading, investing, structured products, lending and so on. Retail is driven by retail deposits and retail lending, but generally, corporate activities are the bedrock of the banking sector.

The strategies of large commercial banks are tested by competition and fuelled by technological innovation in IT and the advent of AI, at a time when the economic environment is weak. Most of them are looking at ways to fend off competition by acquiring promising fintech startup companies.

Grey areas between the historically well-defined segments are getting wider with IT and AI blurring the borders between traditional banking, digital banking and fintech companies.

The rise of Capitec and changing brand dynamic

Technology and the increased use of internet banking steered large commercial banks to close many branches, with the cost, rent and salary savings deemed considerable enough to proceed. The functionality of centralising the monitoring of operations and rectifying transactions changed the banking experience.

Now customers visiting a branch must still phone the appropriate department in head office to resolve issues. The newcomer on the South African banking scene, Capitec, followed a slightly different logic, offering a narrower range of services, which account for 90% of banking transactions, in smaller size branches.

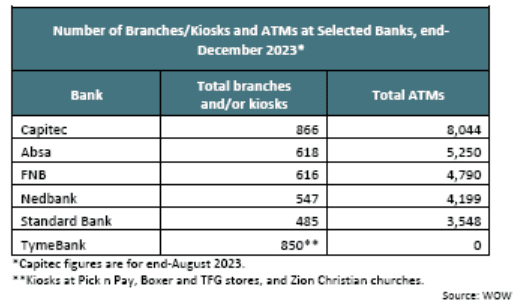

Capitec chose to increase its branches and ATMs, which proved to be a successful strategy, contrarian to the historical large banks’ strategies.

Since opening for business on 1 March 2001, Capitec went from 55 branches and 25,000 clients to more than 840 branches and 15,000,000 clients in 20 years.

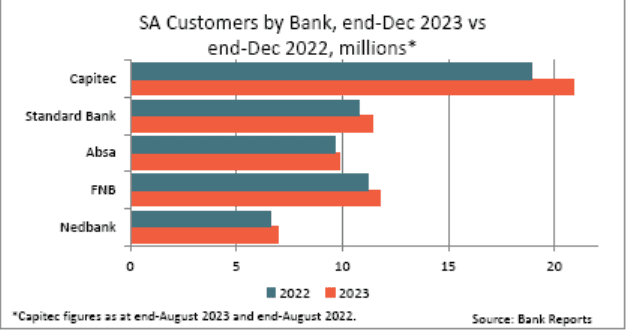

The table below shows a comparison of number of customers vs branches and ATMs of the major banks.

The price:earnings ratio of the banks show that the market values Capitec higher than any of the major banks. This is despite the fact that Capitec has the lowest Tier 1 capital buffer, and is thus exposed to higher risk of volatility. Capitec’s P:E stands at 24.8 while the big four P:E range is between 11.1 and 6.4.

Newcomers in the financial sector

Traditional banks do provide digital banking, which is increasingly becoming the channel of choice for banking transactions, but their physical branch network continue to exist, enabling a wider range of services. Those services do not account for banks’ volumes and profits.

In South Africa, three new players have entered the arena of digital banking – Bank Zero, TymeBank and Discovery Bank. They are all digital banks as they do not have any physical retail outlets network, but provide standard banking services. They offer a bank account, debit card, transfer and withdrawal services. By 2023, TymeBank had over 8.5 million customers, Discovery Bank 2 million and Bank Zero over 700,000.

TymeBank and Bank Zero, as the latter’s name implies, focused on low and zero bank account fees. TymeBank’s go-to-market strategy is through Pick n Pay retail outlets, where they have installed terminals. Their message is that customers open their account at these terminals, and can withdraw and deposit cash at PnP tills, a commercial arrangement that was part of their strategy. Cost leadership and convenience of essential service elements created greater differentiation. Discovery Bank followed a different strategy, targeting upmarket customers with a smaller base, but higher costs, sold on the perception of prestige.

Fintech companies represent the next wave of entrants into the financial sector. Capitec CEO Gerrie Fourie stated that he is not afraid of competition from another bank like the one launched by Old Mutual, but rather of companies like Apple.

Possibilities, accessibility, and portability of smartphones are almost endless. Terms like “wallets” encapsulate what is coming. People have a wallet on their phone where money is stored and can be transferred to another phone wallet of a customer or beneficiary directly from one phone number to another, with very low to no transaction costs.

There is a growing trend of telecom providers offering banking services and lifestyle services with the likes of Vodacom extending transactions with lending facilities, with the launching of Vodalend for personal and small business loans in partnership with Old Mutual. These trends are well articulated in the WOW report on the banking industry.

The missing but not impossible link for mass penetration in rural South Africa is a convenient, easily accessible, and cost-effective channel for cash deposits and withdrawals, driving demand in the retail sector through the likes of Pick n Pay for TymeBank and Spar for Bank Zero.

Technological innovation benefitting the mass consumer market with lower cost, easier, and portable financial services indeed makes the fintech players the next competitors for commercial banks.

Is there a need for a state bank?

In this context, the question of establishing a state bank is still to be answered. If government was to adopt more progressive models like the one implemented by the likes of TymeBank, underserved rural areas could get access to financial products not offered by mainstream banks.

Unfortunately, the government has not demonstrated technical capability to establish a bank. Careful planning and oversight to ensure accountability, efficiency, and financial sustainability are key ingredients which the government does not seem to have in place.

Ultimately, the decision to pursue a state bank should be guided by a comprehensive assessment of its potential benefits and risks, considering the evolving dynamics of South Africa’s financial landscape and the imperative of promoting inclusive economic growth.

Confectionery, often referred to simply as sweets or candy, holds a special place in the hearts and palates of consumers worldwide. With sugar and cocoa as its main ingredients, the confectionery industry provides various indulgent treats, from chocolates and candies to pastries and marshmallows.

The South African confectionery industry is dynamic and vibrant, and continues to evolve to meet the needs of consumers, although it faces challenges such as rising ingredient costs and competitive pressures.

The Power of Sensory Experience

The allure of confectionery lies in its ability to evoke tempting aromas, vibrant colours, and irresistible flavours, creating a multisensory indulgence for consumers.

Whether savouring a decadent chocolate truffle or enjoying a tangy gummy bear, confectionery products captivate the senses and provide moments of joy and pleasure. This sensory experience forms the foundation for brand differentiation and consumer loyalty in the competitive confectionery market.

Brand Differentiation and Premium Pricing

Successful confectionery brands leverage their unique sensory experiences to differentiate themselves in the marketplace and maintain premium pricing. Iconic brands like Nutella have achieved enduring success by offering singularly successful flavour profiles that resonate with consumers.

Lindt, a Swiss chocolate brand known for its premium quality ingredients and artisanal craftsmanship, commands higher pricing despite intense competition from conglomerates like Cadbury and Nestlé. The singular focus of Lindt on chocolate production allows it to prioritise quality and innovation, distinguishing itself from competitors with diverse product portfolios.

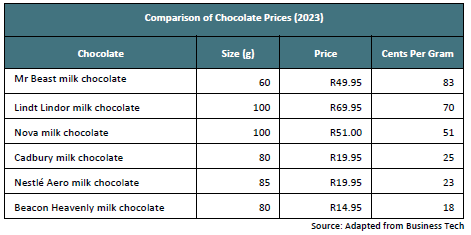

More broadly, as illustrated in the WOW report on The Confectionery Industry in South Africa, some well-known chocolate brands in South Africa have pricing that is vastly different on a cost per gram basis as illustrated in this table:

Competitive Landscape in South Africa

In South Africa, the confectionery industry faces challenges posed by rising sugar and cocoa prices, changing consumer preferences, and competitive dynamics. Premium brands like Lindt may face pressure to maintain market share as cost-conscious consumers seek cheaper alternatives.

Conglomerates like Cadbury and Nestlé, with diverse product offerings beyond confectionery, must balance brand management and resource allocation across multiple categories. This complexity can impact brand focus and market positioning, affecting competitiveness in the confectionery segment.

The Biggest Trend Driving Competitiveness

One of the biggest trends contributing to competitiveness in the South African confectionery industry is the shift towards healthier and more sustainable products. With increasing consumer awareness of health and wellness, brands that offer sugar-free, reduced-sugar, and ethically sourced confectionery options are gaining traction.

By innovating with alternative sweeteners, natural ingredients, and eco-friendly packaging, brands can appeal to health-conscious consumers and differentiate themselves in the market.

Conclusion

The South African confectionery industry offers a tantalising array of indulgent treats that captivate consumers’ senses and evoke moments of pleasure. Successful brands differentiate themselves through unique sensory experiences, premium quality ingredients, and strategic branding.

However, in a competitive landscape shaped by changing consumer preferences and economic factors, brands must adapt to emerging trends, prioritise innovation, and maintain consumer trust to stay ahead of the curve. By embracing trends in health, sustainability, and sensory innovation, confectionery brands can navigate challenges and seize opportunities for growth and success in the dynamic South African market

The role of telecommunications in driving economic development

Telecommunications serves as a backbone of modern economies and underpins various industries that are essential for economic activities, from financial services, software development and ecommerce to media and entertainment. Telecoms operate in the backroom of what are considered the magnificent seven viz. Apple, Amazon, Alphabet, Microsoft, Meta, Tesla and Nvidia. Nvidia is known for its contribution to AI acceleration, edge computing and virtualisation found in telecommunications technologies.

While companies such as Nvidia are driving new technologies, access to and distribution of all information generated, including by AI, is via telecommunications in mobile, fibre or traditional fixed line operations. Telecommunications companies haven’t shared the limelight with the magnificent seven, but are equally important to sustain the progress in software development.

Unlike AI and software development, which rely on human capital, telecommunications is more capital intensive.

Challenges in the African telecommunications industry

In Africa, challenges of access and insufficient telecommunications infrastructure remain, with some remote areas still not covered by terrestrial infrastructure, mostly affecting low to middle income groups, and consequential lower spending in less densely populated areas means the expected return on high capital investment remain relatively low. However, it is notable that the sector has seen great progress in Africa with over 1.1 billion unique mobile subscribers in 2020, accounting for around 84% of the population covered by mobile networks. Telecommunications continues to play a crucial role in driving economic development across the continent.

The availability of the latest ICT infrastructure in African countries is however still lagging. For example, as reported in WOW’s ICT and Telecommunications Industry in Ghana report, 3G is widely used on 90% of voice calls, with latency (delay in establishing connection) poor in most cases. MTN and Vodafone offer 4G coverage 66% and 54% of the time respectively. This is representative of most African countries on the higher end of the development scale, as Ghana is relatively well positioned in relation to other African countries.

Addressing the digital divide

The digital divide is still a reality on the African continent, where a lack of digital literacy and technical skills inhibits the effective adoption and utilisation of new technologies. Education systems are still grappling with adequately preparing students with the digital skills needed to thrive in technology-driven economies, limiting opportunities for innovation, entrepreneurship, and technology adoption.

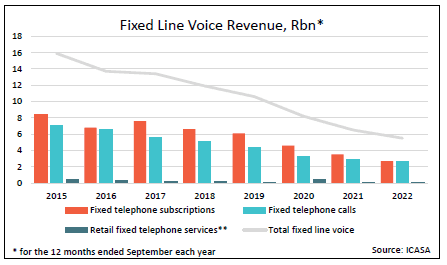

South Africa, as the most industrialised country in Africa, ranks well in telecoms availability as it has benefited from huge investments by private sector operators. This is illustrated in the WOW report on Telecommunications and Retail of Electronic Devices in South Africa, which includes the graphs above.

Competitiveness in South Africa’s telecommunications sector

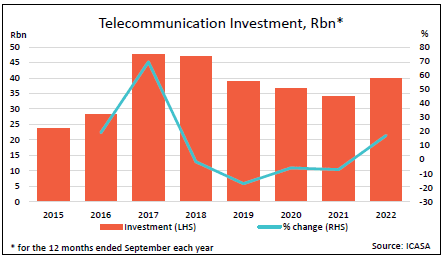

Revenue growth has followed this investment, but ongoing technological developments and innovation will require continued investments in, for example, 5G and fibre connections. Telkom’s legacy fixed line voice revenue continues to decline, as illustrated in the graph above, restricting its ability to fund new investments.

Openserve (owned by Telkom) has approximately 165,900km of fibre optic network cable, followed by Vumatel with around 50,000km, meaning that Telkom has three times Vumatel’s network and yet according to information in the WOW telecommunications report, Vumatel has the largest network by homes passed (households that have access to a particular network) at 2 million, while Openserve announced over 1.1 million homes passed by June 2023.

According to a report by Africa Bandwidth Maps, as of June 2023, the total length of operational fibre optic network in South Africa was 1,279,026km, increasing by 36.6% from 936,102km in 2018 and 143.7% from 524,847km in 2013. The report said an additional 94,998km of fibre optic network entered service in the 12 months since June 2022, an average of 260km of new fibre optic network per day.

Conclusion

The sector has been plagued by regulatory inefficiencies and delays in migrating from analogue to digital broadcasting, with government missing an opportunity to avail infrastructure opportunities that could have contributed to economic activity among the small players in the sector. Despite the challenges, it is evident that there is resilience and competition that fosters innovation and drives the expansion of network infrastructure. It is not unreasonable to infer that this is driven by the money to be made.

In the wider sense, telecommunication has been and continues to be a significant engine for GDP growth and wealth creation for individuals with better and wider access to communications via smartphones and other devices, which can provide people in rural areas access to the internet, and market places for products and services.

South Africa can look forward to even better and faster access and affordability of telecommunications.

Introduction

Information on the healthcare sector is plentiful and summarised in the latest WOW report on the healthcare sector in South Africa.

Besides the issue of the relatively large number of qualified doctors whom the Department of Health (DoH) cannot absorb in the system despite the shortage of doctors due to budget constraints, the key topic dominating media reports and public discourse is the National Health Insurance (NHI). Why is it so controversial?

National Health Insurance

Government’s fixation on NHI needs some debunking. A few high-level numbers offer some insights and highlight the percentage of health budgets versus spent per person in South Africa.

The private medical aid spends rounded R30,000 per member per annum for about 9 million people; the public sector spends only R5,500 per person for 51 million people. The discrepancy between the two has to do with the quality of healthcare being provided through a multitude of channels, private doctors, specialists, healthcare professionals, private clinics and hospitals who all have some cost base. So how is the government going to deliver quality healthcare to all 60 million people? Even if it can somehow reduce the cost from say R30,000 as it currently stands in the private sector to say R23,500, it would have to spend an extra R18,000 on 51 million people currently part of the public sector healthcare delivery. It would mean an additional spending of more than 900bn on healthcare.

The South African Government already runs a very high budget deficit of 4.9% of GPD, adding to the already high levels of debt at over 70% of GDP. Increasing taxation on individuals even if the NHI is implemented in stages would become excessive. The sentiment conveyed in the press is also that medical doctors and healthcare specialists are not enamoured with the NHI with some seriously thinking of greener pastures on more welcoming countries which would cripple NHI’s capacity to deliver when South Africa already has a shortage of doctors and nurses.

South African healthcare spending compared to other countries

Comparing South African health spending with other countries lays bare inconsistencies and the utter ineffectiveness of public sector healthcare management.

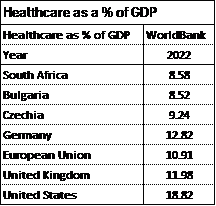

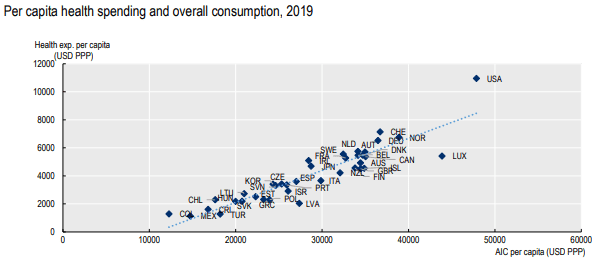

South Africa spends about the same percentage of its GDP on health as central European EU member states, yet the service delivered is unmistakenly different. Many countries in a similar spending range as South Africa provide better and more universal healthcare. The US is an outlier, spending much more than any other country as confirmed in the OECD table below. The OECD study about “Understanding differences in health expenditure between the United States and OECD countries of September 2022” did not provide a clear answer as to why, especially given that the quality of care does not differ from other develop countries listed.

Not so evident from the statistics is that the UK, which has a national healthcare system that would closely resemble South Africa’s proposed NHI, does not have a good record of service delivery according to the British Journal of Nursing. The Journal further states that they have seen several Never Events in NHS England (2023) where wrong procedures took place, or the wrong patient was treated

Source: OECD

Locally, WOW highlights maladministration, poor maintenance and corruption on a grand scale, including lack of protection for whistleblowers, in the public health sector as the main cause of poor service delivery.

Is the NHI the best model for South Africa?

While the NHI aims to provide healthcare coverage that addresses disparities, the implementation of such a system requires a concerted effort to address existing challenges such as maladministration and inefficiencies to utilise the high spending in a manner commensurate with service delivery, ahead of extending public sector management to the entire healthcare industry in South Africa.

A blended solution, as found in many developed countries, combining innovation and efficiencies of the private sector with broader public sector funded model might be beneficial to address the inequalities in the South African economy.