The possibility of a power shift from Eskom and renewables producers in South Africa

One cannot discuss the South Africa power crisis and electricity generation without focusing on Eskom, a longtime monopoly operator that remains the dominant supplier. The organisation is a prime example of how rent-seeking and loss of competitive behaviour creep in to the extent that efficiency and productivity can seem impossible to regain, especially when there is no competition.

The Truth About Eskom Load Shedding

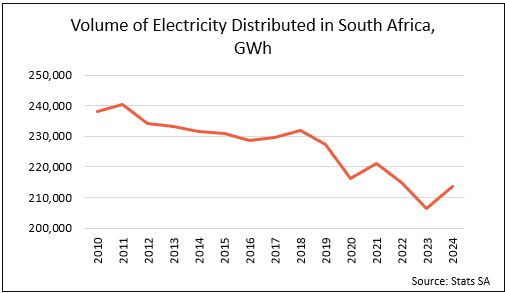

Recent gains have been lauded as great achievements, such as the 352 loadshedding-free days reported in Eskom’s financial report to end-March 2025. The Who Owns Whom report on the generation of electricity in South Africa reports that Eskom had a marked turnaround from just 36 loadshedding-free days in the previous year. On the face of it, this is remarkable, but there is continued load reduction and curtailment, extensive use of expensive diesel-fueled open-cycle gas turbines and declining sales (183TWh in 2024 from 188TWh in 2023). The decline is offset by renewable energy as shown here.

As reported in MyBroadband on 29 September, Eskom praised the completion of Unit 6 of its Kusile power station as “within the planned timeframe” when in fact it is the most expensive coal power station ever built with costs having gone up from the initial R80bn to about 460bn and its completion being 11 years LATE.

The tragedy is that the high cost of Eskom power has spilt over into the entire economic fabric, manifesting in consistent low growth over the years as industries were impacted by high input costs, resulting in stagnation in the new project pipeline. Eskom’s excessive tariff increases have even worried the South African Reserve Bank (SARB), as they are making it difficult for the SARB to win the inflation fight and therefore preventing lower interest rates for consumers.

The current status at Eskom

The absence of drastic measures to address real problems and the deflection of costs onto consumers through exceptionally high tariff increases have made Eskom uncompetitive, especially against renewable energy South Africa projects promoted by the private sector, which, despite difficult circumstances and obstructionism, has become cheaper every year.

The slow pace of liberalisation of electricity generation and the unbundling of Eskom’s monopoly is holding the full potential of the investment in and growth of renewables back.

What can be done to address power generation in South Africa?

Eskom can be more progressive in this approach rather than continuing to be protectionist by defending its old way of doing business. The unbundling and liberalisation have been adopted as government policy, and if all public entities in the industry were to enforce this transition and fully collaborate, the power generation challenges could be overcome. This anti-competitive behaviour by Eskom has a negative impact on the economy.

For South Africa to regain competitive electricity pricing in support of its economy, a truly independent transmission company with its own infrastructure assets needs to get off the ground and make the transmission of electricity from new generation locations a reality. This will enable new renewable energy players to supply electricity to end-users at significantly lower rates, forcing Eskom to become more competitive.

Can Eskom return to being the lowest-cost electricity supplier?

From the outside, it appears that Eskom has several options to regain competitiveness and become a price leader without burdening users with high tariffs. Here are a few suggestions:

- Financial and workforce restructuring to reduce operating costs;

- Increase GWh sales per employee by increasing energy availability factor (EAF); the South African old coal-fired power stations with an EAF of 62.66% YTD need to match those similar ones in the US that have an EAFs of 90%+;

- Find ways to deal with the municipal debt of R94bn; and

- Open the door wider to private sector participation in new renewable, storage and gas projects.

This would be a good start toward reducing tariffs and making Eskom competitive. Eskom must also accommodate more renewables to facilitate the transition to greener generation and compliance with export markets.

In the words of the IMF, apply bitter medicine to get well and look forward to a brighter future for the benefit of all South African citizens. Their well-being should be the primary focus.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries Electricity gas steam and air conditioning supplySouth Africa

South Africa’s Maritime Sector: Growth, Green Tech & Global Competition

Contents [hide] There is no doubt that the maritime transport sector is an important keg in the South African economic wheel. According to the Who Owns Whom report on maritime...

BlogCountries Electricity gas steam and air conditioning supplySouth Africa

The Energy Sector in Namibia: Projects, Investment & the Drive for 80 % Local Supply

Contents [hide] Namibia’s move towards reducing energy import dependency Who Owns Whom’s report on the energy sector in Namibia highlights the country’s forward-looking economic development policy addressing its dependency on...

BlogCountries Electricity gas steam and air conditioning supplySouth Africa

Can Independent power producers turn the tide in electricity generation for South Africa?

Contents [hide] The complexities of power generation in South Africa As detailed in our recent report on the generation of electricity in South Africa, Independent power producers have become indispensable...