South Africa’s mining decline and its impact on economic growth

Continued trend in the South African mining industry

It is clear that South African mining production has been in decline for quite some time, a critical issue for the mining of precious metals in South Africa, although mineral resources are far from depleted. Who Owns Whom’s report on the mining of precious metals and minerals in South Africa indicates that precious metals exports increased by 10.1% in 2024 due to the increased price of gold, improving the performance of the mining industry despite the continued production decline.

The inevitable questions to ask are why the decline continues, and what does government need to do differently to reverse this trend? In the words attributed to Einstein, insanity is doing the same thing over and over and expecting different results.

Importance of the mining sector to South Africa

Despite the continued decline in production, the mining sector remains a vital component of the South African economic landscape. The decline has been evident in the diminishing contribution to GDP from around 20% in the 1980s to 8.3% in 2013 and 6.2% ten years later. A loss of 2.1% of South Africa’s GDP of R7.024tn in 2023 represents R147.5bn in lost economic activity, according to data from Statistics South Africa.

In 2023, South Africa’s formal employment stood at about 11.5 million. Applying the ratio of employment to GDP to the lost output, about 241,500 direct jobs never saw the light of day. The tragedy is that the loss in economic activity and value add creation can never be recovered. There is however remedy, especially given the wealth of mineral resources still in the ground, and one would imagine that the government would prioritise the revival of this important industry, a priority that on the surface seems straightforward.

Volatility of precious minerals pricing

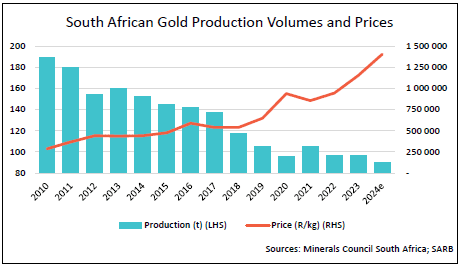

South Africa should not delay actions to revive this industry because the recent high gold price in South Africa and globally has masked the real impact of the decline in actual production, as illustrated in the graph. In the present climate of increasing conflict between nations, the gold price is unlikely to drop a lot in value, regardless of the consistent oversupply for years.

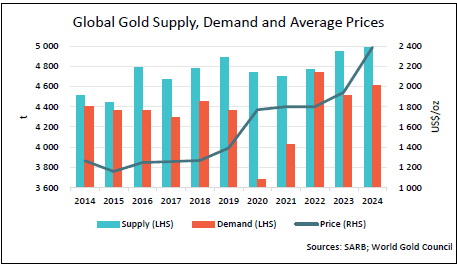

Gold has kept its very special status as a safe haven among investors worldwide. Central banks hold trillions of dollars’ worth of gold in their safes and, according to the World Gold Council, keep adding to it. This gives gold a privileged status compared to platinum group metals (PGMs), of which South Africa has the highest reserves worldwide. Without the same standing, the PGM market in South Africa and globally is much more tied to a supply-demand market equilibrium, so these metals lag gold in pricing power.

Geopolitical shifts and associated consequences

Recent political turmoil has seen a sharp upward movement in PGM prices in the last few months, impacting the PGM price outlook. These circumstances may change, but South Africa should not wait for it to happen in a world where competition can cause major damage to market shares, as shown with its gold production over time, more so than for other metals due to unwavering demand for the metal.

Safe havens change in nature over time. For example, the gold standard, with gold backing the US currency, was cancelled in 1933, while in 1971, the convertibility of US currency for gold was abolished. Today the value of the US currency is backed by the US economy, not by its gold reserves. Also, cryptocurrencies are making headway as an investment and transactional alternative, offering the advantage of convenience and flexibility that gold does not possess. The minting of gold coins for daily transactions as a medium to exchange goods is distant history.

Market forces

In recent times, developing nations have started increasing the pressure to maximise the value of their mineral and metal resources extracted by foreign companies on their land, and to advance beneficiation in their countries. South Africa has been talking about beneficiation for decades now, but has not brought this to impactful fruition. This approach has been lauded as advancing economic growth for many countries. High reserves and low extraction costs can create some leverage for a while, but with a decade-long lack of foreign direct investment in mining in South Africa, it is clear that government needs to urgently improve on its policies and create a more certain investment climate to curb the continued downward trend and the consequential loss to the economy and employment.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries Mining and quarryingSouth Africa

The Role of Service Activities in South Africa’s Mineral Sector

Contents [hide] The mining industry has long been a cornerstone of South Africa’s economy, with associated services being essential and critical in the value chain. The WOW report on services...

BlogCountries Mining and quarryingSouth Africa

Illegal mining – an explosive nuisance

Contents [hide] Illegal mining has grown exponentially in recent years in South Africa, as detailed in WOW’s report on the Manufacture of Explosives and pyrotechnics in South Africa . The...

BlogCountries Mining and quarryingSouth Africa

Can the South African mining industry continue to grow following Covid?

Contents [hide] The mining industry in South Africa is one of the biggest contributors to the country’s fiscus, and one would imagine it to be on government’s priority list for...