A snapshot of Botswana’s financial services industry

A comparison between the financial services industry in Botswana and other middle-income countries

The financial services sector in Botswana is similar to other middle-income countries like South Africa. According to Who Owns Whom’s report on financial services in Botswana, the industry is characterised by a mix of commercial banks, microfinance institutions, pawnshops, savings and credit co-operative organisations (SACCOs), foreign exchange bureaus, a notable presence of mobile money services and the rising fintech segment. The relatively new mobile money and fintech industries are rising fast. This is despite the country’s conservative governance and strong regulatory environment that contrasts with more liberalised peers, where innovation is faster but sometimes riskier (like Kenya or Nigeria).

The difference between commercial banks and development finance institutions (DFIs) is that the DFIs’ main activity is lending, while the commercial banks carry out both lending and transactional services. Transactional banking has regained importance due to technological advances.

Growing role of digital banking

Physical handling of cheques and transfer forms required a significant labour force to verify and correct entries, but these physical tasks have largely been replaced by technology. This has lowered costs and improved the profitability of managing and transacting for client accounts. Wells Fargo in the US was substantially fined and restricted for years, for opening unsolicited multiple accounts for clients just to multiply transaction fees. Consequently, the valuation of banks has shifted back from merchant/investment banks to more traditional, previously undervalued retail/transactional banks.

Technology has opened new avenues for transacting and competition, with new products finding a receptive market. Mobile money, a product enabled by the mobile communication infrastructure of telecoms companies, has seen significant growth. The Who Owns Whom report states that in 2024, mobile broadband subscriptions grew by 16.0% to 2.9 million from 2.5 million the previous year, and recorded a CAGR of 6.81% from 2018 (1.5 million) to 2024, facilitating increased access to financial services throughout the country.

Fintechs have sprung up to offer similar services using existing internet infrastructure. With limited infrastructure investment, fintech companies can compete on cost while providing the convenience and improvement in financial access for underserved populations, especially youth and informal sector workers.

Major players in Botswana’s financial services sector

The four largest Botswana commercial banks are all foreign-owned. The advantage of this is that the technology is transferred from parent companies, making transacting costs minimal with the support of the international banking groups. This eventually benefits the people of Botswana.

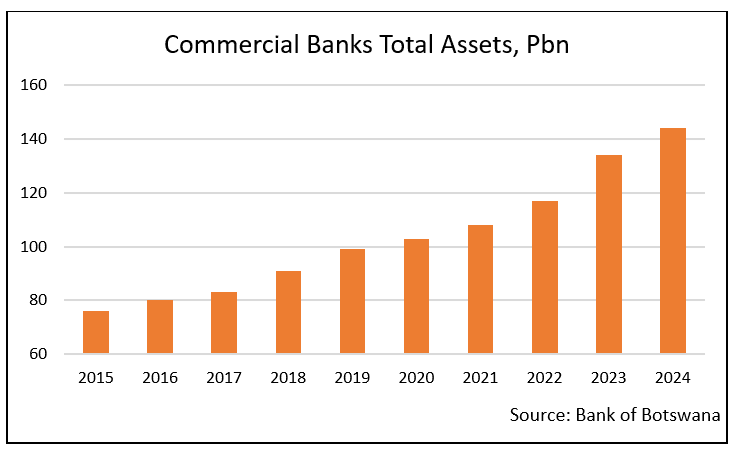

The standing, fiduciary quality and stability from conservative governance, and strong regulatory environment of major banks keeps these institutions competitive. According to the Who Owns Whom’s report, as of December 2024, commercial banks’ total assets were P144bbn (US$10.3bn), rising by 7.5% from P134bn (US$9.9bn) in 2023. The report further details the composition of the various peripheral entities in the financial industry [and can be found here].

Microlenders’ business grew by 125%, and pawnshops’ loan books by 47.6%. No reliable data appears to be available for mobile financial transactions, as they are connected to mobile subscriptions that underwent a cleanup of inactive numbers.

Botswana is still largely rural with only two towns, Gaborone and Francistown. The country’s economy, on which the banks rely, continues to show good growth. According to Who Owns Whom’s report, the real GDP growth rate was 11.9% in 2024 from 3.2% in 2023. Unfortunately, a contraction of 4% in 2025 is predicted by the IMF, due to the country’s dependence on diamonds. The cyclicality of commodities poses a risk for the country’s economy, compelling its government to find ways to diversify the economy and mitigate commodity price volatility.

The financial sector is robust and will continue to grow, although the rate of growth will be strongly influenced by the larger economic impacts caused by commodity prices until a degree of diversification is found.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries Financial and insurance activitiesSouth Africa

Cryptocurrencies and security dealing activities in South Africa

Contents [hide] The main players in securities dealings and South Africa’s position The rise of cryptocurrencies has introduced new dynamics in securities dealing, challenging traditional financial markets and regulatory frameworks....

BlogCountries Financial and insurance activitiesSouth Africa

The development of flexible and customised insurance products in South Africa

Contents [hide] Life insurance as a business Life insurance is unlike many other businesses in that it has an uncertain future cost associated with the income it generates from premiums,...

BlogCountries Financial and insurance activitiesSouth Africa

The rise of new competition in the South African banking sector

Contents [hide] The financial services sector in South Africa stretches from the South African Reserve Bank to micro lenders, cooperative banks, stokvels and loyalty programmes that have become popular for...