The rise of new competition in the South African banking sector

The financial services sector in South Africa stretches from the South African Reserve Bank to micro lenders, cooperative banks, stokvels and loyalty programmes that have become popular for customer engagement and enhancement of services. This is articulated in the WOW report on the banking industry in South Africa.

Banking, as experienced or aspired to by citizens, has been mainly carried out by the five largest banks – Standard Bank, First National Bank (FNB), Nedbank, Absa, and Investec, which collectively held 89.5% of total banking sector assets at end-March 2023, and increasingly by newer entities manifesting as simplified low-cost banking such as Capitec, digital banks such as TymeBank and Bank Zero, and pure fintech companies, with some of them backed by large corporates such as Vodacom.

Commercial banks present and future

Commercial banks essentially have two legs, retail and corporate, with the latter including business banking, advisory services, trading, investing, structured products, lending and so on. Retail is driven by retail deposits and retail lending, but generally, corporate activities are the bedrock of the banking sector.

The strategies of large commercial banks are tested by competition and fuelled by technological innovation in IT and the advent of AI, at a time when the economic environment is weak. Most of them are looking at ways to fend off competition by acquiring promising fintech startup companies.

Grey areas between the historically well-defined segments are getting wider with IT and AI blurring the borders between traditional banking, digital banking and fintech companies.

The rise of Capitec and changing brand dynamic

Technology and the increased use of internet banking steered large commercial banks to close many branches, with the cost, rent and salary savings deemed considerable enough to proceed. The functionality of centralising the monitoring of operations and rectifying transactions changed the banking experience.

Now customers visiting a branch must still phone the appropriate department in head office to resolve issues. The newcomer on the South African banking scene, Capitec, followed a slightly different logic, offering a narrower range of services, which account for 90% of banking transactions, in smaller size branches.

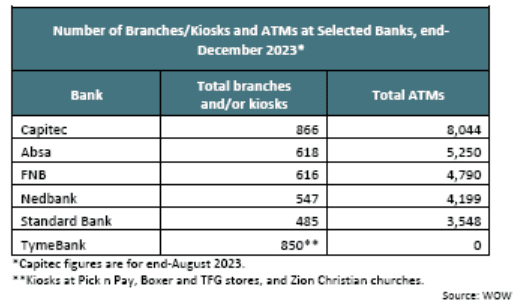

Capitec chose to increase its branches and ATMs, which proved to be a successful strategy, contrarian to the historical large banks’ strategies.

Since opening for business on 1 March 2001, Capitec went from 55 branches and 25,000 clients to more than 840 branches and 15,000,000 clients in 20 years.

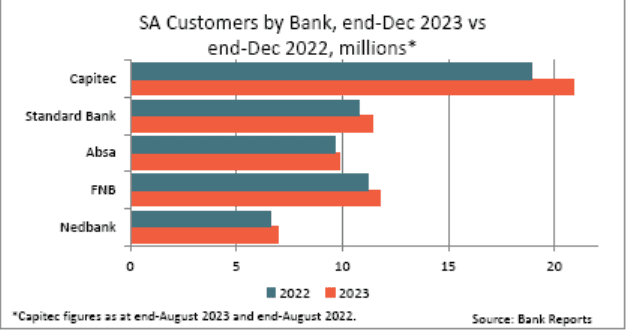

The table below shows a comparison of number of customers vs branches and ATMs of the major banks.

The price:earnings ratio of the banks show that the market values Capitec higher than any of the major banks. This is despite the fact that Capitec has the lowest Tier 1 capital buffer, and is thus exposed to higher risk of volatility. Capitec’s P:E stands at 24.8 while the big four P:E range is between 11.1 and 6.4.

Newcomers in the financial sector

Traditional banks do provide digital banking, which is increasingly becoming the channel of choice for banking transactions, but their physical branch network continue to exist, enabling a wider range of services. Those services do not account for banks’ volumes and profits.

In South Africa, three new players have entered the arena of digital banking – Bank Zero, TymeBank and Discovery Bank. They are all digital banks as they do not have any physical retail outlets network, but provide standard banking services. They offer a bank account, debit card, transfer and withdrawal services. By 2023, TymeBank had over 8.5 million customers, Discovery Bank 2 million and Bank Zero over 700,000.

TymeBank and Bank Zero, as the latter’s name implies, focused on low and zero bank account fees. TymeBank’s go-to-market strategy is through Pick n Pay retail outlets, where they have installed terminals. Their message is that customers open their account at these terminals, and can withdraw and deposit cash at PnP tills, a commercial arrangement that was part of their strategy. Cost leadership and convenience of essential service elements created greater differentiation. Discovery Bank followed a different strategy, targeting upmarket customers with a smaller base, but higher costs, sold on the perception of prestige.

Fintech companies represent the next wave of entrants into the financial sector. Capitec CEO Gerrie Fourie stated that he is not afraid of competition from another bank like the one launched by Old Mutual, but rather of companies like Apple.

Possibilities, accessibility, and portability of smartphones are almost endless. Terms like “wallets” encapsulate what is coming. People have a wallet on their phone where money is stored and can be transferred to another phone wallet of a customer or beneficiary directly from one phone number to another, with very low to no transaction costs.

There is a growing trend of telecom providers offering banking services and lifestyle services with the likes of Vodacom extending transactions with lending facilities, with the launching of Vodalend for personal and small business loans in partnership with Old Mutual. These trends are well articulated in the WOW report on the banking industry.

The missing but not impossible link for mass penetration in rural South Africa is a convenient, easily accessible, and cost-effective channel for cash deposits and withdrawals, driving demand in the retail sector through the likes of Pick n Pay for TymeBank and Spar for Bank Zero.

Technological innovation benefitting the mass consumer market with lower cost, easier, and portable financial services indeed makes the fintech players the next competitors for commercial banks.

Is there a need for a state bank?

In this context, the question of establishing a state bank is still to be answered. If government was to adopt more progressive models like the one implemented by the likes of TymeBank, underserved rural areas could get access to financial products not offered by mainstream banks.

Unfortunately, the government has not demonstrated technical capability to establish a bank. Careful planning and oversight to ensure accountability, efficiency, and financial sustainability are key ingredients which the government does not seem to have in place.

Ultimately, the decision to pursue a state bank should be guided by a comprehensive assessment of its potential benefits and risks, considering the evolving dynamics of South Africa’s financial landscape and the imperative of promoting inclusive economic growth.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries BotswanaFinancial and insurance activities

A snapshot of Botswana’s financial services industry

Contents [hide] A comparison between the financial services industry in Botswana and other middle-income countries The financial services sector in Botswana is similar to other middle-income countries like South Africa....

BlogCountries Financial and insurance activitiesSouth Africa

Cryptocurrencies and security dealing activities in South Africa

Contents [hide] The main players in securities dealings and South Africa’s position The rise of cryptocurrencies has introduced new dynamics in securities dealing, challenging traditional financial markets and regulatory frameworks....

BlogCountries Financial and insurance activitiesSouth Africa

The development of flexible and customised insurance products in South Africa

Contents [hide] Life insurance as a business Life insurance is unlike many other businesses in that it has an uncertain future cost associated with the income it generates from premiums,...