Namibia’s move towards reducing energy import dependency

Who Owns Whom’s report on the energy sector in Namibia highlights the country’s forward-looking economic development policy addressing its dependency on imports, which currently account for between 40 % to 60 % of its energy requirements. It plans to produce 80 % of its own energy by 2030.

Latest policy signal: the International Energy Agency notes a government target “to generate 80 % of electricity domestically by 2028” Achieving this goal would sharply cut electricity imports from South Africa and the Southern African Power Pool and position Namibia as a net exporter within SADC.

Namibia’s GDP per capita and its approach to energy generation

Despite its geographical expanse, Namibia is a small and low-income country. It has a population of only 3 million people, and it ranks 122 out of 189 IMF-measured countries with a GDP/capita of US$4,711, while South Africa is ranked 108 at US$6,517, and Mauritius scores top with a ranking of 76 at US$13,099.

According to the IMF DataMapper ( , Namibia’s GDP-per-capita has hovered around US$4,700-US$4,900 since 2022, underlining the need for diversified energy-led growth.

It has offered oil and gas explorers reasonable terms, realising that there is great potential for economic and industrial growth for the country. It is well understood that oil and gas exploration is high risk for any oil major intending to venture into this space, as it involves a huge investment, particularly given the considerable lead time it takes to reach production.

Energy sector hurdles and projects in the pipeline

The challenges are considerable. The pending gas-powered power station feeding from the Kudu offshore field, discovered in 1974, is testimony to the long duration from exploration to production. The BW Energy financial investment decision to implement the 800 MW project has been postponed to 2025, and it will then take another two to three years to reach production and onshore delivery of oil and gas.

Update: Reuters confirms the delay, noting that BW Energy now targets a 2025 final investment decision after revising costs and opting for a floating production unit –

Many other discoveries were made along the Namibian coast in other petroleum exploration blocks, creating highly promising prospects for the oil and gas industry in Namibia, touted to become the fifth largest oil producer in Africa by the middle of the next decade, according to the Who Owns Whom report.

Shell’s Graff-1 (2022) and TotalEnergies’ Venus-1 (2022) finds in the Orange Basin alone could hold >2.5 billion barrels of recoverable resources, propelling Namibia toward an expected 700,000 bbl/d plateau by 2030, according to Reuters.

Most Namibian fields pose challenges as they are 100 km to 300 km offshore, on average, with depth ranges of over 3,000 m, way beyond currently commercially exploited offshore fields. There are also complex rock permeability conditions in some areas. However, advances in technology will continue to be made, as has happened with fracking.

Namibia is taking all this into account and is including technological advances in its preparation for production, and it has commenced investment in the onshore infrastructure in the ports to manage the volumes that will be handled once production is underway.

Contribution of oil and gas exploration projects to the Namibian economy

The oil and gas reserves explored in Namibia have the potential to attract foreign direct investment, with companies like Qatar Energy and the Portuguese energy company Galp already invested. These investments will drive infrastructure development and create high-skilled jobs in engineering, logistics, and trade, contributing to employment among the youth.

The Who Owns Whom report indicates that the country attracted foreign direct investments of US$4.4 bn between 2021 and 2023, of which US$2.0 bn, or 45 %, are linked to the oil and gas industry.

Public data from Namibia’s Investment Promotion and Development Board shows total inflows of N$73 billion (≈US$4.4 bn) in the same period, with N$33 billion directed to oil & gas –

The report also highlighted that the country’s gross fixed capital formation increased by 50.0 % in real terms to US$2.4 bn in 2023 from US$1.6 bn in 2022, largely due to a 237.9 % increase in mineral exploration (which includes petroleum exploration) to US$1.2 bn in 2023 from US$355.1 m in 2022.

Very soon, Namibia, which is currently a net oil and gas importer and consumer of 0.02 Mb/day, will become a producer of 0.7 Mb/d, more than South Africa’s daily consumption of about 0.55 Mb/d.

The business-friendly policies in Namibia have enabled the private sector to participate meaningfully in the economy, creating onshore business opportunities in the SME space.

Energy mix in Namibia

The Namibian energy mix strategy is quite diverse, being made up of solar, gas, wind, biomass, and green hydrogen, with independent power producers’ participation growing and estimated to contribute about 11 % of the national energy mix according to the news in Namibian Mining & Energy. A recent Electricity Control Board update cites 23 IPPs investing N$5 billion to date.

Oil and gas production is not supported by international energy transformation policies but will remain an essential source of energy and an input to many chemical, pharmaceutical, and other industries.

Complementing hydrocarbons, the flagship Hyphen Green Hydrogen Project aims to export up to 300,000 t of green hydrogen annually from Namibia’s Kharas Region – positioning the country as a future renewable-fuel hub.

The different energy projects underway in Namibia put the country well on its way to achieving the 80 % local production and reducing its energy dependency.

Events such as conferences were organised very differently in the 1990s compared to now. Simple examples such as confirming attendance and enhancing value for delegates have resulted in drastic improvements in attendee experience.

Globally, technology has transformed the management of events and attendance, participation and the value-add realised from events. The shift toward hybrid formats was propelled by the pandemic, which fast-tracked advancements in digitisation. From big global summits to smaller, more focused product launches, one can attend online, in-person or through a combination of the two. The integration of artificial intelligence (AI) and virtual reality (VR) have enhanced the experience, engagement and efficiency for event organisers.

Competitiveness of the South African event management industry

South Africa’s event management industry has remained competitive, particularly business, conferences and large-scale exhibitions. The country has world-class venues, established infrastructure, a good climate, and a good reputation for hosting big events.

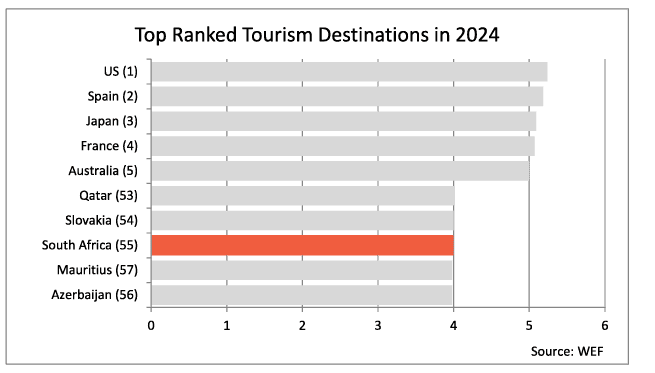

According to the Who Owns Whom report on the event management industry in South Africa, the country is the highest-ranked conference destination in Africa, with Cape Town ranked the top convention city in Africa. The G20 summit is taking place in the country and the minister of Sports, Arts and Culture, Gayton McKenzie, announced that he would bid for a Formula 1 race to be hosted at Kyalami again. Given that the country hosted the 2010 FIFA World Cup, the Rugby World Cup in 1994, and the Netball World Cup in 2023, the chances of being awarded a Formula 1 race seem probable.

The meetings, incentives, conferences and exhibitions (MICE) industry contributed R121.8bn to the economy in 2023 and is poised to grow with its integration of technology, sustainability, investments, digital transformation and tourism recovery strategies.

The graph indicates the potential for growth and the stiff competition the event management industry faces. If the issues stated below are addressed, South Africa is well placed to improve its ranking and draw some of the opportunities from countries which currently have a better ranking.

Challenges facing South Africa’s event management industry

the country needs to address several issues for it to take advantage of the positives mentioned above. As competition from the US and Europe is growing, urgent attention to some of the issues highlighted in the Who Owns Whom report on event management are required.

The technology projects underway to address visa issues need to be accelerated, especially issues affecting tourism from countries like India, Nigeria, and China. There is potential to attract high volumes of tourists from these countries, so streamlining visa issuance will unlock value.

Water and electricity shortages are still hindering the industry, with event visitors expecting venues to have solutions to these problems. Big venues have invested in alternative power and water supplies, with the CEO of Gallagher Convention Centre being quoted saying it has secured a 1 million litre back-up water supply on the property.

Another issue that is being addressed is the air connectivity hurdle. As a long-haul destination, South Africa, through the Department of Transport, has developed a national air access strategy with Cape Town.

Geopolitical shifts and their impact on event management

The world is facing various geopolitical challenges and South Africa is not immune to them. Ongoing wars and conflicts in Ukraine, Gaza and Yemen, and annexation threats to Greenland, Panama Canal and Canada by the US have resulted in instability and uncertainty which may lead to less long distance travel and affect the event management industry.

The industry in South Africa can still grow if the issues highlighted in the Who Owns Whom report are addressed adequately and timeously.

Who Owns Whom’s report on the wholesale and retail of food in South Africa highlights critical shifts in the industry amid ongoing debates about VAT increases. With food security and inequality at the centre, private sector innovation and government policies are reshaping the landscape, particularly in township economies and the growing ecommerce sector.

The VAT increase in the latest Budget is considered insensitive to low income earners, and insufficiently offset by an extended exemption of additional food items to avoid the likelihood of deepening poverty, inequality, and injustice.

Challenges in South Africa’s food wholesale market

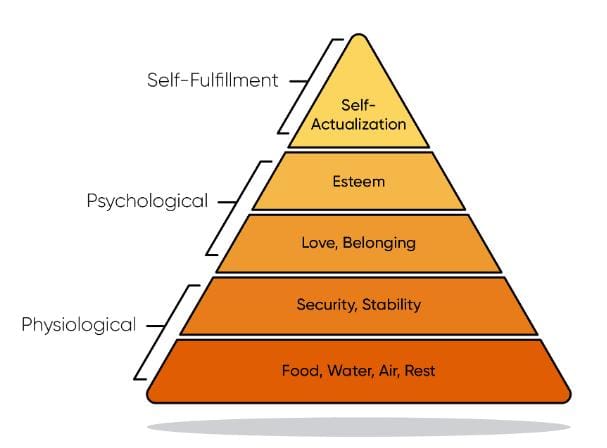

Food is the most basic need and at the bottom of the Maslow hierarchy, ahead of clothing and shelter. With a stagnating economy and rising cost of living, the plight of lower-income earners and the unemployed, and their daily need for food, cannot be ignored.

Stats SA’s unemployment figures crept up from 26% to over 30% from 2015 to 2020 and have stuck well above 30% since then while real unemployment, using an expanded definition, sits above 40%, which is unacceptably high and deserving to be a primary priority for any government.

Food production and wholesale in South Africa

There has been an increase in small-scale food production, which is not very productive due to supply chain hindrances, making it difficult for small producers to gear up for the export market. Small-scale production is key to improving food security for households.

Some of the biggest retailers such as Shoprite, Pick n Pay, Spar, and Food Lover’s Market have expanded their presence in townships, rural areas and low-income communities. They have also started to form partnerships with informal traders, such as spaza shops, to streamline supply chains and improve product availability, thereby enhancing the food wholesale and distribution network within township economies and making hygienic food more accessible for poor communities

Operational efficiencies, hygienic standards and financial standing are enhanced through these partnerships and contribute to lowering food prices. These initiatives were mostly spurred by the entry of foreign wholesalers mainly from Pakistan, Somalia and Ethiopia introducing cheap foodstuffs into the community, challenging incumbent retailers to find innovative ways of remaining profitable while serving this huge market, which is estimated in the billions of rands.

Regulation in the food retail sector

For the longest time, spaza shops operated informally and did not have to comply with regulations, mainly because they are spaza, meaning miniature or imitation of the real thing. The R638 Food Regulations introduced in 2018 to help ensure that all food products are safe for human consumption, has not been adequately monitored and enforced to the extent that fatal casualties occurred. Government reactively decided to introduce further regulations that call for each spaza shop owner to rezone their home or place of business and register it as a business within a short timeframe. It however then displayed woeful incapacity to deal with the applications. This new regulation has been costly for applicants and does not address hygiene and food safety issues that were plaguing the industry.

Private sector resilience and self-regulation

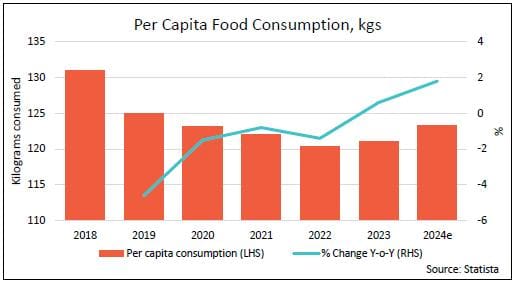

South Africa’s continued development of new shopping centres is testimony to the private sector’s ability to find ways to thrive in a stagnant economy. Despite years of declining GDP/Capita, food consumption is increasing, indicating that nutritional intake is improving to some extent.

An example of how the private sector self regulates is how Pick n Pay’s shareholders, who paid a heavy price for poor management, supported a turnaround plan, subscribed to a rights issue and changed management. No taxpayer funds were involved in this “business rescue” as at a critical stage, Pick n Pay was technically insolvent. If it had no reasonable prospects, bankruptcy and liquidation would have ensued, at no cost to taxpayers.

Growth of ecommerce grocery sales South Africa

As articulated in the Who Owns Whom report on the retail of food in South Africa, the rapid growth of ecommerce and home delivery services has seen retailers increasingly adopting sophisticated technologies and fulfilment models.

There are great successes and innovations in this sector despite some challenges pertaining to food security, inequality and affordability for millions of South Africans.

The status of travel and tourism in South Africa

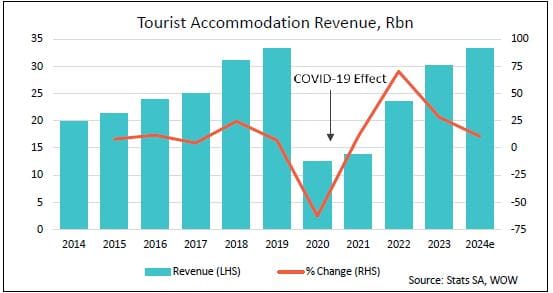

The drastic COVID-19 lockdown measures were devastating for tourism industries all over the world, as illustrated in the graph below on South African tourist accommodation revenue, sourced from Who Owns Whom’s report on Travel and Tourism Trends in South Africa.

It is devastating that four years on, South Africa has not really caught up with pre-pandemic tourism levels in terms of numbers of tourists and revenue. Statistics do not always convey the magnitude of the loss for a country, particularly for small tourism operators, employment, foreign exchange inflows and even fiscal revenues. In 2020 alone, more than R20bn evaporated.

South Africa’s tourism industry challenges

External events over which the country has little, or no control can create havoc. Natural causes like volcanic eruptions in Iceland have the potential to direct tourism to far flung destinations like South Africa, while others like the pandemic can have devastating effects. Draconian visa regulations on international travel can seriously damage tourism. For example, the recent US-Canada tariff war is resulting in a significant drop in Canadian tourists crossing into the US. According to the Caribbean News Digital website, An Ipsos poll found that 65% of Canadians plan to avoid travelling to the United States. This shift can result in several billions of dollars loss in revenue for the US hospitality sector.

Geopolitical tensions or power struggles between countries or regions that affect international relations, economic stability and global security can lead to a drop in tourism.

The impact of regulation on the travel and tourism industry

Regulations can be burdensome, and compliance requires time, funds, and resources that can sometimes constitute an insurmountable barrier for small startups to get off the ground.

According to a Stanlib article on business regulation scores, South Africa was ranked last with the highest number of regulations for doing business. Looking at the impact of tourism illustrated below, the need for less regulation is clear.

Examples of cumbersome regulations include training requirements for the tourism industry which state that a tour guide must be registered with provincial tourism authorities and must complete a training course through a training provider accredited by the Culture, Arts, Tourism, Hospitality, and Sport Sector Education and Training Authority (CATHSSETA).

It is questionable whether this profession needs to be overregulated. In a freer business environment, competent competition would wipe out a bad tour guide, as demand is driven by discerning tourists and intermediaries like travel agents. There is no need to force a training course on a tour guide.

Opportunities and future growth

Despite the country’s economic and recent geopolitical hiccups, South Africa’s tourism industry has great potential for growth. The country is endowed with excellent climatic conditions and tourist attractions such as game reserves and national parks, nature reserves, botanical gardens, wildlife sanctuaries, cultural and natural heritage sites, wine farms, craft breweries and distilleries, museums, historical landmarks, art galleries, beaches and aquariums.

Rethinking the approach to increasing regulation is becoming urgent in a country with sky-high unemployment. A freer operational environment in the tourism industry help to attract potential tourists locally and internationally.

As tourism is one of the most labour-intensive industries globally, more support and less regulation can unlock this powerful driver of employment. Its ability to generate various opportunities in numerous industries such as transport, entertainment, retail and wine tourism demonstrates the importance of this industry.

Now that Spain and other popular destinations are protesting against the influx of tourists, perhaps South Africa can use this as leverage and show that it welcomes tourists any time.