South African Mining Industry Trends Report – July 2022

The minefield that is a goldmine?

How did South African Mining do?

The WOW report “South African Mining Industry Trends Report – July 2022” brims with easily and quickly grasped graphs that bring home three strong themes we will go over. Starting with the sector’s good performance despite difficulties in the regulatory environment, followed by the sector’s contribution to the South African economy, and thirdly, reflect on the windfalls that the South African government could have perhaps prioritised for the mining sector – and not simply assume that the high commodity prices will last forever.

The WOW report rightly states that South Africa is still a mining country. The sector is estimated to have the world’s 5th largest mining sector in terms of GDP value. It is an indispensable foreign exchange earner maintaining a large trade surplus over a number of years. Mining exports in 2021 contributed almost 50% to the export basket.

The SA Mining sector’s contribution to the economy

This sector is simply a goose that keeps laying the golden egg for South Africa and is a great benefactor to the government, through taxes, levies and royalties. It has kept trade in surplus and supported the Rand value by contributing about R441 billion. Without mining exports, South Africa would face a deficit of R 379 billion. This industry also makes significant contributions of over R 95.2 billion to the fiscus. This is the good part of the story

The SA Mining sector’s resilience over time

The South African mining sector keeps performing well and has shown incredible resilience, despite fatal accidents and strike action for more than 100 years. The resilience has sometimes been helped by international economic circumstances that drive up commodity prices as witnessed in recent years when most sectors suffered huge setbacks due to the Covid pandemic and the Ukraine-Russia war further exacerbating supply chain challenges.

What could have been expedient, was the regulatory and infrastructure support by government. During the previous commodity boom (ca 2010-2012), South Africa only benefitted a fraction of what other “mining” countries realised and has receded into the perverse situation where the interventions have become entirely negative. The loss of income is now far larger than what could have been the cost incurred by the government in the form of infrastructure investment required. The consequences are also not automatically reversible.

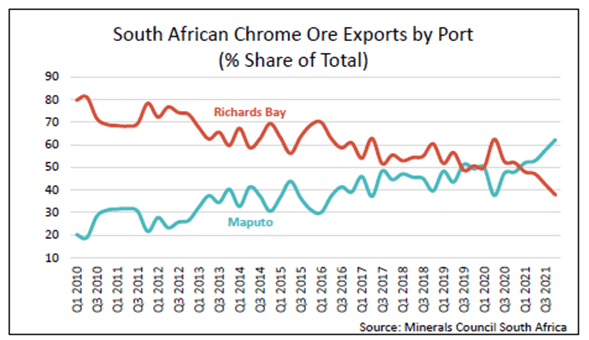

The WOW graph on chrome exports below illustrates the point. The efficiency of the Maputo port over Richards Bay outweighs the time-consuming border crossing between SA and Mozambique. Now that this export route has gained strong traction, it will take some convincing for companies to return to the South African ports.

The problem is not limited to chrome mining. Many minerals like manganese, copper and iron mining face the same export challenge, whilst coal mining with the Richards Bay allocations has even bigger export challenges,

The other source of concern of course emanates from the non-supportive regulatory environment created by the Department of Minerals and Energy (DMRE). Their unacceptably long approval process and delays with 4,000 applications pending, say it all. This is not good news, especially given that these applications relate to NEW exploration and mining rights which could result in much-needed investments both local and Foreign.

What the SA mining sector requires for it to grow

The statistical information relayed in the WOW report indicates that currently, fixed investments in the mining sector are largely restricted to maintaining current operations, with new mining investments visibly absent.

This of course takes us to the tremendous windfall for the economy and the government at the most opportune time during the Covid-19 pandemic that enabled the government to offer a relief grant of R350 to the poorest communities. Even if the commodity prices stay high, the sudden huge benefit will not last forever. Economies will go through a period of painful adjustments before reverting to a balance of prices and income for all sectors and groups in the economy because of oil price surges aggravated by the war in Ukraine.

It would be good if Government were to incentivise this sector to continue realising the benefits stated above by investing in much-needed infrastructure. South Africa is ranking very low as a mining investment destination and related to this ranking is the bottom ranking in terms of ports efficiency of Richards Bay Terminal, the main gateway for South Africa’s mining exports. This calls for government intervention in working toward the improvement of this lifeblood of the economy to gain a competitive advantage.

The South African mining sector does have a high level of technical and production expertise. With environmental considerations having forced global markets to shift from coal to cleaner options in the future, the DMRE should adapt to these global trends by fast-tracking the issuance of exploration licenses for new minerals and materials in response to growing demand in a changing world economy to replace coal in good time.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

Blog Mining and quarryingSouth Africa

Can South Africa turn its chrome dominance into industrial power?

Contents [hide] South Africa’s iron ore and chrome mining sector has benefited from the recent commodity price boom, strengthening export earnings and stimulating new investment. Yet beneath this growth lie...

BlogCountries Mining and quarryingSouth Africa

South Africa’s mining decline and its impact on economic growth

Contents [hide] Continued trend in the South African mining industry It is clear that South African mining production has been in decline for quite some time, a critical issue for...

BlogCountries Mining and quarryingSouth Africa

The Role of Service Activities in South Africa’s Mineral Sector

Contents [hide] The mining industry has long been a cornerstone of South Africa’s economy, with associated services being essential and critical in the value chain. The WOW report on services...