Ports and harbours have evolved from the days when they merchants would display their crafts and fishermen would bring their daily catch, socialise over coffee and exchange their goods. Today, ports and harbours have sophisticated infrastructure with the main activity being facilitating trade, loading and offloading ships.

Ports and harbours are now a complex and integrated hive of activity at the core of supply chains that connect every part of the world. The introduction of containers by to ports catapulted the transportation of goods across international waters.

Challenges at African ports and harbours

With the world being so connected, and ports being the lifeline of trade globally, Africa needs to fast-track the development of its infrastructure for it to achieve the big goals envisaged through the African Continental Free Trade Area (AfCFTA) Agreement.

The Who Owns Whom report on ports and harbours in Africa highlights some of the challenges Africa is grappling with, such as inefficiencies and cargo handling backlogs, port congestion, vessel scheduling issues, container shortages and soaring freight costs.

Opportunities in global shipping are also hampered by security threats, particularly attacks perpetrated by Houthi militants in the Red Sea, and piracy off the Horn of Africa and in the Gulf of Guinea.

Environmental sustainability in the ports industry

Climate change-related issues resulting in weather-related risks are some of the challenges to be addressed to avert port delays and disruptions.

There is a growing need for green ports, renewable energy integration, and practices that align with environment and sustainability goals. The lack of the latest technologies, and poor road and rail infrastructure in some African countries provides those countries an opportunity to implement the latest technologies and utilise green materials that were not in the mix for developed countries.

Investments and projects in African ports

The Who Owns Whom report refers to some of the investments across the African continent, with two major investors being the UAE and China. The UAE’s “One port one node” strategy aims to establish a network of ports connecting the Gulf with Africa. It has also invested in African port infrastructure and port operations, primarily through DP World and the Abu Dhabi Ports Group (AD Ports).

China is the largest investor in African ports and harbours, with at least 61 existing or planned port projects in Africa, funded, built and/or operated by Chinese entities and financed by the Export-Import Bank of China (China Exim Bank) and China Development Bank.

Maersk through its subsidiary, APM Terminals, one of the world’s largest port companies, is also planning to invest in new terminals in East and Southern Africa.

These initiatives demonstrate that Africa is taking centre stage in terms of investment, which is not surprising given its size and the minerals available on the continent that are in demand globally.

How is technology shaping African ports?

The graphic below indicates how complex ports have become, and without the use of technology and sophisticated systems, such operations could be almost impossible.

Some African countries like Kenya, South Africa, and Morocco have already invested in advanced cargo tracking and single window systems with automated clearance processes improving efficiency, and clearance times and ensuring transparency.

Ports Value chain

Opportunities in the African port industry

With the many infrastructure gaps and the lack of digital infrastructure like high-speed internet, there is plenty room for public private partnerships, while the need to address the shortage of skilled workers capable or operating and maintaining advanced systems offers more opportunities.

Port modernisation can be realised through mutually beneficial partnerships and collaboration that could harmonise systems within regional trade blocs such as the AfCFTA.

The liquor industry, like the tobacco industry, has been a prime target for raising taxes (with little resistance from the public) and restrictive advertising rules. The country imposes what are called sin taxes because of liquor’s addictive qualities. Tobacco is more addictive and thus subjected to much more pervasive and brutal regulation than alcohol.

The country ranks fifth globally in terms of alcohol consumption per capita with approximately 30 litres per person consumption per annum.

The impact of restricting alcohol consumption and high taxes

Restrictions and high taxes, including excise duties, aimed at curbing high consumption and liquor-related harm are not very effective.

The readiness of people to pay whatever they can for these products is obviously a clear signal for the government that it can raise the level of sin taxes significantly without much pushback.

The problem, however, exists in that excessive taxes constitute another form of restriction and trigger illicit trade. The additional restrictions during COVID invigorated illicit distribution channels. But as the saying goes: “Things that have never happened before, happen all the time”, and illicit alcohol, which accounts for about 20% of the market in South Africa, is a dangerous product if the wrong alcohol is produced, as happened in Laos recently, resulting in several fatal casualties.

Excessive taxes result in illicit alcohol trade, reduced profit margins for legal producers, and heightened financial pressure on consumers.

Market segments of the liquor industry in South Africa

The consumption of liquor in South Africa varies based on factors such as socioeconomic status, cultural norms, and urban-rural divides. In more affluent urban areas, the trend is toward moderate consumption of premium alcoholic beverages like craft beer, fine wines, and spirits, often associated with social and leisure activities.

Lower-income and rural communities tend to consume cheaper alcoholic products, including home-brewed, partly due to affordability issues. The youth and young urban professionals show a growing preference for trendy, flavoured beverages and pre-mixed, ready-to-drink cocktails. At the same time, traditional African beer remains popular in rural and township communities, often coupled with cultural rituals and social gatherings.

The size of illicit liquor trade in South Africa

According to the WOW report on the liquor industry in South Africa, a report released in 2020 by the South African Liquor Brand Owners Association, the Beer Association of South Africa, and the wine industry association Vinpro estimates that illicit alcohol sales (counterfeit and unlicensed products) grew at a CAGR of 17% between 2017 and 2020. In 2020 illicit sales were estimated to be R20.5bn or 12.2% of total industry sales (which the report estimated at R177.2bn) which remains a key concern for the industry. This illicit trade includes smuggled goods, counterfeit alcohol, and homebrews, with significant public health risks and destabilisation of the legal alcohol industry.

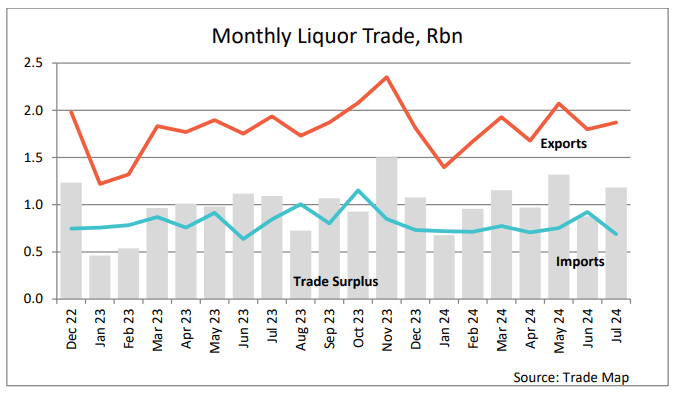

Liquor imports and exports

The liquor industry’s trade surplus, as indicated in the graph, paints a positive picture despite the decline in wine exports, which dropped by about 17%, primarily due to logistical bottlenecks at Cape Town port and rail infrastructure issues. For the country to claw back and recover lost markets, it needs to improve its infrastructure network. The industry should be able to leverage its strong relationships with international buyers and recover its exports.

Despite challenges associated with taxes and regulation, smaller player can capitalise on various opportunities, by choosing niche markets such as craft beer, premium spirits, or traditional beverages while embracing sustainable practices like eco-friendly packaging or organic production methods, to serve growing consumer demand for responsible products. They can also leverage existing local networks and engage in community-based marketing to thrive in this competitive market that is heavily taxed.

Botswana, a country that is often celebrated as one of Africa’s most stable democracies, has been characterised by consistent economic growth driven by diamond mining, sound fiscal management, and political stability; yet it has struggled to diversify its economy to achieve greater equality. Major policy changes in the agribusiness sector are aimed at improving living conditions and fostering food security.

Botswana’s lay of the land and its agricultural characteristics

As articulated in the Who Owns Whom report on Agribusiness in Botswana, the country’s agriculture sector is dominated by traditional farming systems typified by traditional farming methods, limited use of fertiliser and certified seeds, low mechanisation, limited irrigation, and low productivity. Adding to the challenges of traditional farming, Botswana’s crop production is low due to its semi-arid climate and low soil fertility.

Botswana is a relatively small country with a heavy reliance on mining. Its diamond industry in particular is key for GDP growth. In recent years, the diamond market has not fared too well with a decline in volumes traded and pricing. This contributed to a 3.6% drop in the country’s GDP in 2023.

While the agriculture sector only contributes about 1.6% to GDP compared to 14.2% from mining and quarrying, it provides a livelihood for most citizens who operate subsistence farms.

Policy changes introduced in the agricultural sector

David Ricardo’s theory of comparative advantage explains an economy’s ability to produce a particular good or service at a lower opportunity cost than its trading partners. It does not account for artificial advantages created by financial, industrial and technological means overpowering marginal natural advantages.

In January 2022, Botswana’s government introduced a ban on the importation of fruit and vegetables to balance trade, enhance local production and improve food security. This measure is more drastic than raising import tariffs but has resulted in the desired outcome of higher local production.

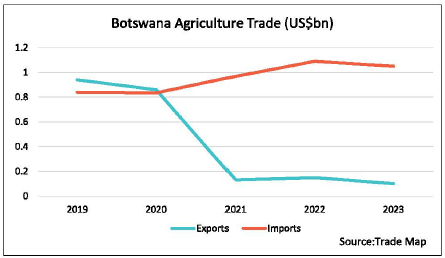

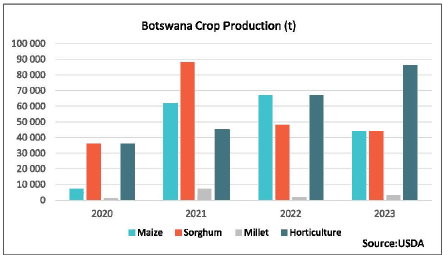

The dramatic growth in Botswana’s agricultural trade deficit and trade restrictions due to Covid-19, as illustrated in the graph above, and the poor diamond export performance made it sensible to decide on an import ban in a sector that provides a livelihood to many. The crop production graph illustrates how this has benefited horticulture which, as a subsector is less prone to price competition from large-scale production, improved substantially.

Implications of the import ban on vegetable growing

According to Who Owns Whom’s report, the ban has reduced the import bill for vegetables by 74.7% to P168m (pula) in 2023 from P634m in 2018, and Botswana is now producing 70% of national demand (of 20,000t per annum) up from 49% before the ban.

Fortunately, Botswana is not a major player on the international scene and will not attract the wrath of international aid agencies who prefer liberal trade, made conditional to aid agency interventions.

A more progressive approach might be a better option, especially for developing countries with limited means to invest in new technologies that produce productivity advantages. This should, however, be with the proviso that the country needs to keep fighting and investing its way up in the competitive landscape so that over time, niche markets can trade competitively internationally.

Most of the approximately 125 million tonnes of solid waste generated in South Africa annually ends up in landfill sites. This should be of concern to all the country’s citizens.

Population growth versus services delivered

Refuse removal service is delivered to fewer households than those recorded between 2010 and 2018 and is non-existent in informal settlements and impoverished urban areas, resulting in the proliferation of illegal dumping sites, littering, and open burning of waste.

There are two glaring realities associated with this problem. One is the available opportunities for job creation and small business development that can result in positive economic activities, and the other is the impact on the environment, ocean life, and quality of water.

There was increased awareness about the status of our oceans during the pandemic, when everything and everyone was grounded. A disturbing documentary showed a turtle being rescued with a straw stuck in its nose. The question that came to my mind was how many other animals get hurt and die due to littering?

How South Africa compares to other countries on waste management

When one looks at how other countries are addressing increasing waste, it becomes clear that South Africa is lagging, particularly considering we have a very progressive National Environmental Management: Waste Act and strategy with circular economy principles with the following intentions.

- Waste minimisation: 45% of waste to be diverted from landfill within five years, 55% within 10 years and at least 70% within 15 years, leading to zero waste going to landfill.

- Effective and sustainable waste services: All South Africans to live in clean communities with waste services that are well managed and financially sustainable.

- Compliance, enforcement and awareness: Mainstreaming of waste awareness and a culture of compliance, with zero tolerance of pollution, litter, and illegal dumping.

A sore sight in cities

Any city dweller in South Africa has witnessed the proliferation of waste pickers who rummage through waste to find valuable materials such as glass, cardboard, paper and plastic for selling.

The Labour Research Service indicated that South Africa’s potential to be the world leader in a just transition for waste pickers is at risk because of weak implementation, monitoring, and enforcement.

Opportunities in waste management

The business sector, through enterprise development and social responsibility initiatives, has the potential to move away from only paying a handful of registered waste pickers by finding creative ways to bring smaller waste pickers into the system, particularly because they are clearly prepared to go to areas many consider to be dangerous.

It is heart-wrenching to see that municipalities themselves, instead of finding ways of formalising waste pickers and remunerating them fairly, would rather issue tenders that only benefit a few.

Who Owns Whom’s report on solid waste management in South Africa indicates that the waste industry value chain generated an estimated revenue of R36.4bn in 2023, with municipalities collectively billing around R6.4bn for refuse collection services. The sector provides more than 30,000 formal jobs and supports an estimated 90,000 informal jobs. This is not a small industry.

As the country struggles to create jobs with a stagnating economy, one wonders why the government does not capitalise on this opportunity and provide much needed dignity to hard-working members of society such as the waste pickers.

While the country struggles with weak enforcement, illegal dumping, and under-serviced communities, other nations such as India’s waste-to-energy plants showcase how innovative policies and technologies can transform waste into value.

Cooperatives and associations in Brazil

Brazil’s government regularised the waste picking operation through cooperatives that provide fair wages, collective bargaining power and social benefits.

Brazil’s waste pickers association advocates for their rights and inclusion, enabling a transition from informal, exploitative conditions to dignified, structured employment.

The examples and opportunities are endless for South Africa to learn from. What is required is the will to tackle the challenge whilst creating employment and ensuring a cleaner and safer environment to live in.